Where are Canadian Interest Rates Heading?

Canadian interest rate expectations are in flux amid higher macroeconomic uncertainty. The Bank of Canada uses the policy rate to meet its mandate target of 2% inflation, so inflation remains within a 1-3% range. Most developed countries have a similar inflation mandate. For the decade prior to COVID, this was a relatively easy task within Western countries, allowing for a period of ultra-low interest rates. However, since inflation spiked across the world post-COVID, inflation management has been a more difficult task for central banks, and Canada is no different. Coupled with the inflation target, the Bank of Canada also seeks to have maximum sustainable employment when conditions warrant. As a result, Canadian interest rates have become a focal point for economists and investors trying to assess the direction of monetary policy.

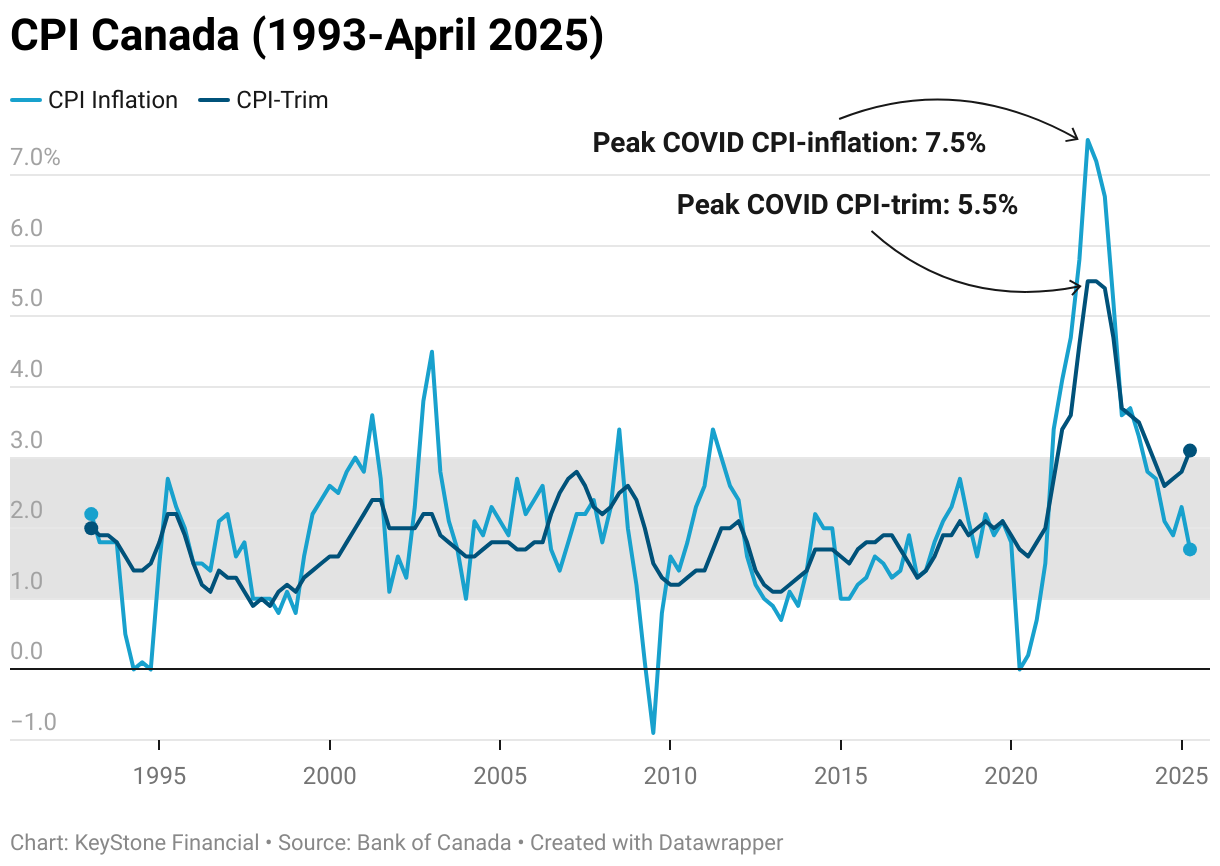

Inflation in Canada – CPI vs Core Inflation

While most news sources will quote total CPI or Headline CPI/Inflation, the Bank of Canada focuses on core inflation. Core inflation removes the impact of more volatile aspects of inflation. CPI-trim is one measure of core inflation, and it excludes the top and bottom 20% monthly weighted price variations. Typically, what gets trimmed are various food prices and energy prices. The Bank of Canada and other central banks commonly rely on core inflation because they can’t control aspects of strong shifts in the supply and demand of products. For instance, a surge of bird flu impacting egg production cannot be solved by monetary policy.

For April 2025 inflation numbers, CPI came in at 1.7%, whereas CPI-trim came in at 3.1%, above the target range. The discrepancy between the two is partially explained by the removal of the consumer carbon tax and decline in global oil prices, which put downward pressure on CPI, but the impact is removed from CPI-trim. The recent increase in core inflation is being attributed to tariffs, which have the potential to structurally increase prices as supply chains shift. This increase in inflation will likely pressure the Bank of Canada to keep Canadian interest rates higher for longer to suppress the impact of inflation. However, this is at odds with the recently weakening employment data.

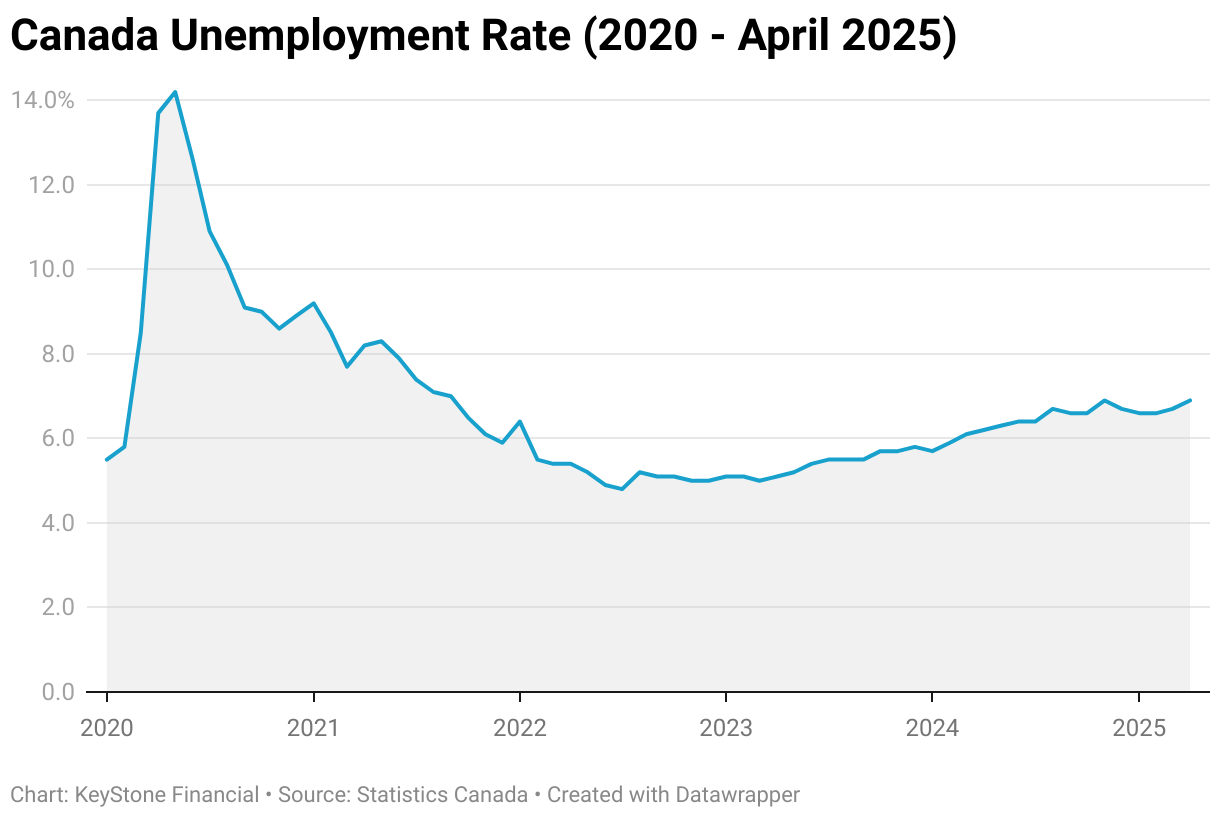

Canada Unemployment Uptick

Canada has seen an upward trend in unemployment since bottoming out in 2022. April 2025 unemployment came in at 6.9%, a monthly sequential increase of 0.2%. A weakening labour market creates a disinflationary effect as household spending decreases as people are unable to find work. Unemployment and Inflation being at odds create a volatile environment for interest rate expectations, as both factors are impacted by interest rate changes. If a central bank increases interest rates to tame inflation, the economy will slow, resulting in increased unemployment. Ultimately, this makes the job of a central bank, like the Bank of Canada, more difficult.

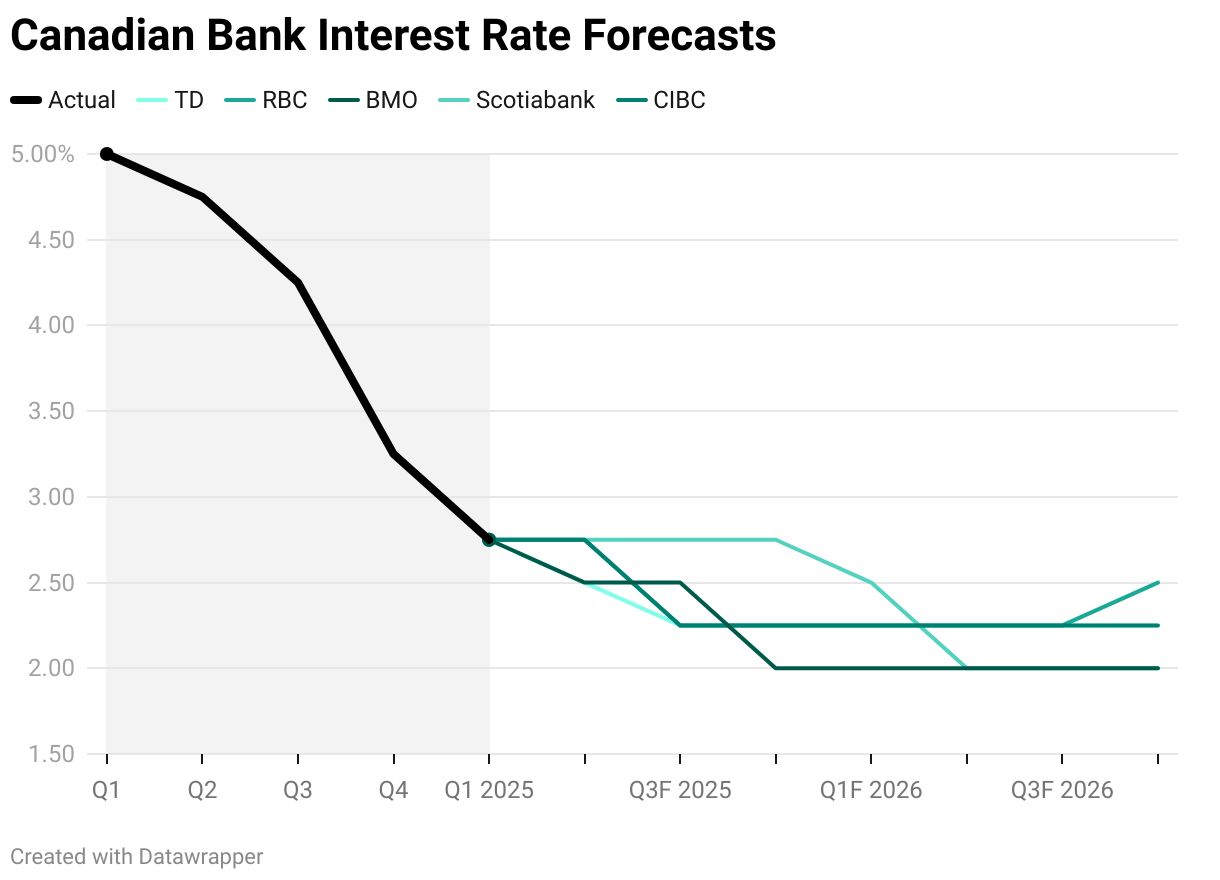

What are Canadian Banks Forecasting For Canadian Interest Rates?

Canada’s policy rate currently sits at 2.75%, a sharp decline from 5.00% just over a year ago.

Due to uncertainty in the Canadian economy, banks have developed significantly different expectations for the policy interest rate. Notably, Scotiabank no longer expects any additional cuts throughout 2025, keeping the rate flat at 2.75%. Scotiabank believes inflation is still too high to support cuts within 2025. ScotiaBank’s Head of Capital Markets Economics wrote, “There is no way that the BoC should be cutting any time soon, if at all “, a marked difference from other banks.

The other big banks all forecast additional cuts throughout 2025 at different cadences. Further, the expectations have been shifting fast, with RBC in April expecting Q2 to end at 2.25% and now a week ahead of the June meeting expecting the rate to remain flat at 2.75%.

This dispersion in expectations, while seemingly small, is notable as banks generally have very similar expectations. The dispersion highlights the uncertainty when it comes to inflation, labour markets and the economy as a whole in Canada. With unclear data, unclear expectations follow.

Data displayed relies on the respective bank’s May Forecasts updated for shifts in end of Q2 forecasts. Some or all forecasts may shift significantly after the next interest rate decision.

Access KeyStone’s Most Recent Update on Geodrill (GEO:TSX)

Updated GEO research report with full analysis of Q1 2025 results, new (BUY/SELL) rating, analysis, and fair value. Do not miss out!

Evolving Dynamics in the Yield Curve

While the Bank of Canada generally (Central banks can use quantitative tightening/easing to influence longer-term rates) relies on adjustments to the overnight/policy rate, many entities rely on longer-term interest rates. The long end of the yield curve has shifted higher despite the short end of the curve trending lower as interest rate cuts occur. The 10-year yield has increased from 3.22% at the start of the year to the current ~3.36%. The longer end of the curve is sensitive to inflation expectations, debt levels, economic growth, capital flows, foreign exchange rates, and other macroeconomic factors. The uncertainty within US trade policy and its international impacts has the potential to impact the long end of the curve substantially as investors weigh the changes.

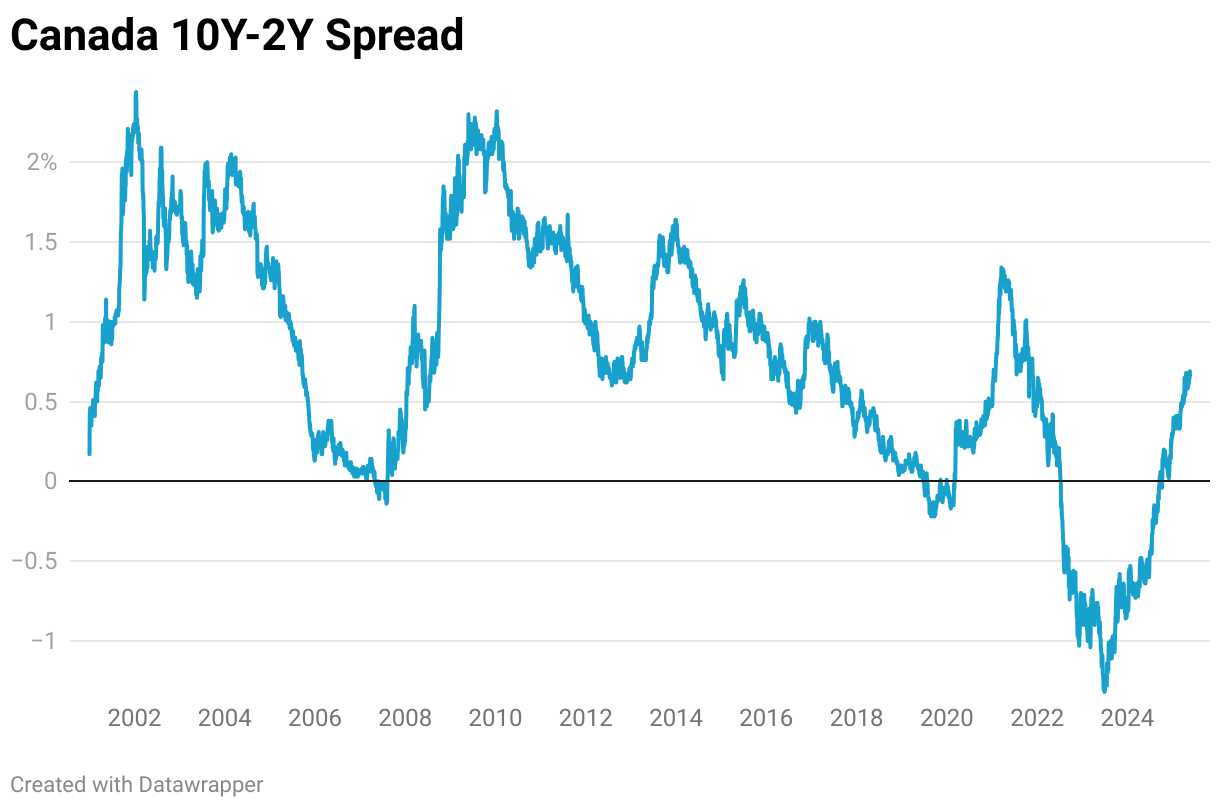

Canadian Yield Curve Term Structure Fluctuations

A bear market steepener is when the spread between the short end of the curve and the long end rises. The dynamic in Canada over the past year has caused a bear steepener to occur as the yield curve uninverted. The yield spread between the 10-year and 2-year bonds has substantially increased over the past year by 126 basis points (1.26%). While the yield curve is now in its normal state of an upward sloping curve, the shift makes long-term financing more expensive not only for the Canadian governments but also for any entity that borrows at long-term rates.

Impact on Companies and Investments

Under higher Canadian interest rates, companies that need to raise capital or currently have outstanding debt will be strained. Interest rate sensitive sectors like real estate and utilities that (generally) borrow on long-term will be required to pay the term premium that has developed or shift to short-term credit if possible, exposing themselves to higher interest rate risk. On the other hand, banks and financial companies which borrow short and lend long can see a benefit in their interest rate margins.

With core inflation still above target and unemployment rising, the Bank of Canada faces a difficult balancing act. As a result, interest rate expectations will likely remain volatile until a clearer trend emerges in inflation, labour market data and US trade policy.

At KeyStone, we are industry agnostic, scouring every single company A-Z in Canada and the US for the best companies, no matter the economic environment. KeyStone recently recommended a company within the financial sector, which has already seen over a 24% return in under 3 months since the recommendation. KeyStone VIP, Canadian Small-Cap and Canadian Dividend clients have access to this research. Click HERE to subscribe and gain access to KeyStone’s game-changing research!