Daily Reset, Long-Term Risk: Why Leveraged ETFs Aren’t Built for Buy-and-Hold

One of the latest financial products being increasingly pushed to the masses is leveraged ETFs, which can offer 2x or 3x the daily returns of the benchmark assets. Leveraged ETFs are increasingly being marketed to the average investor who may not understand the risks of the structured product. Despite having unique risks, leveraged ETFs are being advertised to a mass market.

(Leveraged ETF Advertisements on Reddit.com)

Even though leveraged ETFs are mass marketed they are only suitable as a day-trading tool.

Leveraged ETFs are only reasonable to use within the leverage reset period with only a few exceptions; this is a daily time-frame. The main appeal for traders is the ability to gain access to leverage in a simplified form while not needing to manage leverage through margin loans, futures or options. Effectively leveraged ETFs are simplified access to leverage. Further, leveraged ETFs commonly offer “inverse” options which can provide a leveraged short position, reducing the need to manage a short position.

How Leveraged ETFs Work

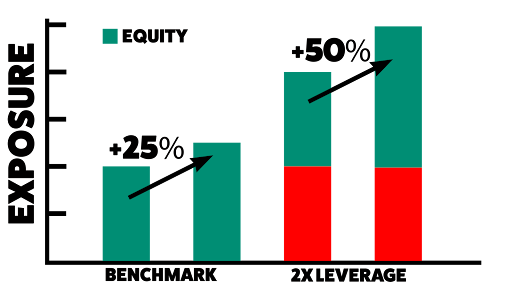

Leveraged ETFs look to leverage the return of a benchmark asset by a multiple normally 2x or 3x. The benchmark assets can be a broad market index like the S&P500, a sector focus like tech,a cryptocurrency like Bitcoin, and more recently single stocks, which is partially why the fund creators love creating leveraged ETFs, the choices are endless. The structure is the same regardless of the benchmark asset but then can be marketed towards various investor groups. The fund creator uses derivatives, whether swaps or futures, to recreate a multiple of the daily return of the benchmark.

If the benchmark asset increased by 25% a 2x leverage ETF will have a return of 50%.

To manage the ETF leverage and stay at the desired leverage like 3x, the leverage needs to be rebalanced, which in leveraged ETF cases is daily. The relatively fixed leverage is in contrast to using other methods to gain leverage which will have variable leverage amounts as the price of the benchmark asset changes. As leveraged ETFs reset daily they start each day at the desired leverage level, which is why they are appealing to day traders, as unless significant intra-day price changes occur leverage should always be approximately the advertised leverage level.

The fixed nature of the leverage is why the risk management side is easier to provide as it is unlikely to have any sort of margin call. Leveraged ETFs offer a simplified structure to historically complex finance products.

Margin Loan Comparison

Under a normal margin loan, with 2x initial leverage the benchmark asset would need to decline 50% over the holding period for the investment to be wiped out (although a margin call would likely occur before), whereas a leveraged ETF would need to decline 50% within one day. Which does sound great, but the leverage resetting to the desired leverage point does however create additional costs.

Volatility Decay

Leveraged ETFs are a disastrous product to use on periods greater than the reset period, and will skew towards negative returns over multiple periods, this is due to volatility decay.

For example, if the benchmark asset falls from $1.00 to $0.95 or declining by 5%, a 3x ETF will fall to $0.85 or declining by 15%. If the benchmark asset the following day rises back to $1.00 or increases by 5.26%, the leverage ETF will increase by 15.79% to $0.984. So, despite the benchmark asset being the same price after the 2 days the 3x leveraged ETF fell by ~1.6%.

The higher the leverage and the higher the volatility the larger the volatility decay will occur, creating a drag on returns over the long term. This can be seen as being short volatility.

Path Dependency

Further, volatility also causes path dependency of returns. In a scenario where multiple days have either negative or positive returns consecutively a leveraged ETF will actually have a better return than non-resetting leverage use like margin loans. However, this does not happen in real markets over anything more than a short period of time.

In this example the benchmark asset increased by 30% over the 6 periods, whereas the 2x ETF increased by 67% and the 3x by 113%, above the 60% and 90% return that would be given by a non-resetting 2x and 3x leverage.

We can contrast this to show path dependency where the benchmark asset (path 2) increases to $1.30 falls back to $1.00 then rises to $1.30 and remains flat. A highly volatile scenario over a 3 day period.

Under this scenario a 3x Leveraged ETF will only rise 11% despite the same ending price as the consistent $0.05 increase in path 1. The path the benchmark asset takes is just as important if not more important than the resulting price.

A bargain for the Fund Manager: High Fees

Like every financial product the creator wants to take a cut, and leveraged ETFs come at a cost. The management expense ratios (MER) are higher, regardless of the benchmark asset type.

While the high expense ratios create a drag on returns, the primary danger for long-term holders comes not from the fees, but from the structural impact of volatility decay.

The worst offenders: Single Stock Leveraged ETFs

Just in 2022, the first single-stock leveraged ETF was launched. Single stock ETFs are some of the poorest performers in a leveraged ETF structure. This is due to the fact that single stocks are generally more volatile than indexes, hence creating more volatility drag.

Real World Results

Looking at the 1-year return for MicroStrategy (MSTR:NASDAQ) and Defiance Daily Target 2x Long MSTR ETF (MSTX:NASDAQ). We can see that despite the benchmark asset, MSTR (in teal), being up ~95% over the past year the 2x ETF (in black) is actually down ~25%.

This shows even if you are directionally correct, using the leveraged ETF over an extended period produces negative returns relative to the benchmark asset. Furthermore we can see a period where the 2x ETF did outperform MSTR, as the stock saw a period of relatively consistent daily increases. But once the consistent period ceased, and relatively sideways movement began the 2x ETF significantly underperformed dramatically. This scenario is the norm for any leveraged ETF products, brief periods of outperformance but underperformance over extended periods.

An Outlier: Leveraged S&P500

A rare outlier since leveraged ETFs have existed are leveraged S&P 500 products. SPXL has surprisingly outperformed SPY over the long term. This is due to the extremely strong performance of the S&P 500 since the bottom of the index in early 2009. This is coincidentally around the same period where leveraged ETFs began launching. In a prolonged period of market drawdown or flat lining, which has happened historically, just not during the lifespan of leveraged ETFs, the leveraged SPX products will dramatically underperform.

Conclusion

Overall, we recommend that investors should stay away from leveraged ETF products, as they are only suitable for intra-trading. Leveraged ETFs are structurally against you due to the volatility decay and path dependency, and only in certain cases will actually result in higher absolute returns. But, this comes at the risk of very significant underperformance when markets are non-directionally flat, generally volatile or move against you. With this in mind the risks outweigh the benefits substantially for any long-term investor.

Instead of high risk and complex financial products, KeyStone helps investors build wealth through building simple 20-25 stock portfolios with low turnover and multi-year holding periods. Learn how to build a better portfolio with KeyStone today.