Firan Technology (FTG: TSX) vs. Simply Solventless (HASH: TSX-V)

A tale of two Small Cap M&A Stock Strategies

Synopsis: Because I feel it valuable to learn our lessons from our portfolio versus a textbook, this article juxtaposes the responsible acquisition strategy of Firan Technology Group Corporation (TSX: FTG) with the more recent aggressive, dilutive approach of Simply Solventless Concentrates Ltd. (TSX-V: HASH), illustrating how their respective paths have impacted shareholder returns. We have interviewed management at both small cap companies. One we have recommended and owned for a decade, the other we took a hard pass on.

Businesses that use a “M&A” as their primary growth driver walk a fine line. For every Boyd Group Services Inc. (BYD: TSX), a serial acquirer of auto repair shops recommended by KeyStone in 2008 at $2.30 which today trades above $200.00, there are ten Dye & Durham’s (DND: TSX) or Lightspeed Commerce’s (LSPD: TSX) – decent business that executed poorly on an aggressive growth-by-acquisition strategy. Unfortunately, the microcap market is also littered with failed or failing M&A strategies, including Simply Solventless Concentrates Ltd. (HASH: TSX-V), which today provides an excellent foil the more measured and successful M&A strategy of Firan Technology Group Corporation (FTG:TSX).

The strategy of growth by acquisition can be a powerful accelerant for a company’s expansion, but its success hinges critically on execution and financial prudence. While an aggressive, debt-fueled, and highly dilutive approach can lead to rapid scale, it often comes with significant integration challenges and shareholder value destruction. Conversely, a measured, responsible strategy, often characterized by strategic debt utilization and minimal share dilution, tends to yield more sustainable and rewarding long-term gains.

While sexy in theory, growth-by-acquisitions can be a risky strategy, with many high-profile examples of mergers and acquisitions failing, often spectacularly. The reality is, a significant number of acquisitions fail to meet expectations, with estimates ranging from 70% to 90%. Common reasons for failure include poor integration, overpaying for the target company, overestimated synergies, cultural clashes, and a lack of strategic alignment.

![]()

Firan Technology Group (FTG): A Blueprint for Responsible Growth

Firan Technology Group (FTG), is a North American manufacturer of high-technology printed circuit boards and illuminated cockpit products for aerospace and defense, exemplifies a disciplined and accretive growth-by-acquisition model. FTG has pursued an opportunistic and measured M&A strategy to expand its capabilities, customer base, and market reach, all while maintaining a strong balance sheet and prioritizing shareholder value through minimal equity dilution.

FTG’s approach often involves:

- Strategic Fit: Acquiring companies that complement existing operations, technology, or market segments.

- Debt for Acquisition, Cash for Repayment: Utilizing debt to finance acquisitions, then aggressively paying down that debt through robust operating cash flows from the combined entities. This avoids diluting existing shareholders by issuing new shares.

- Effective Integration: A strong focus on integrating acquired businesses to realize synergies and optimize operations.

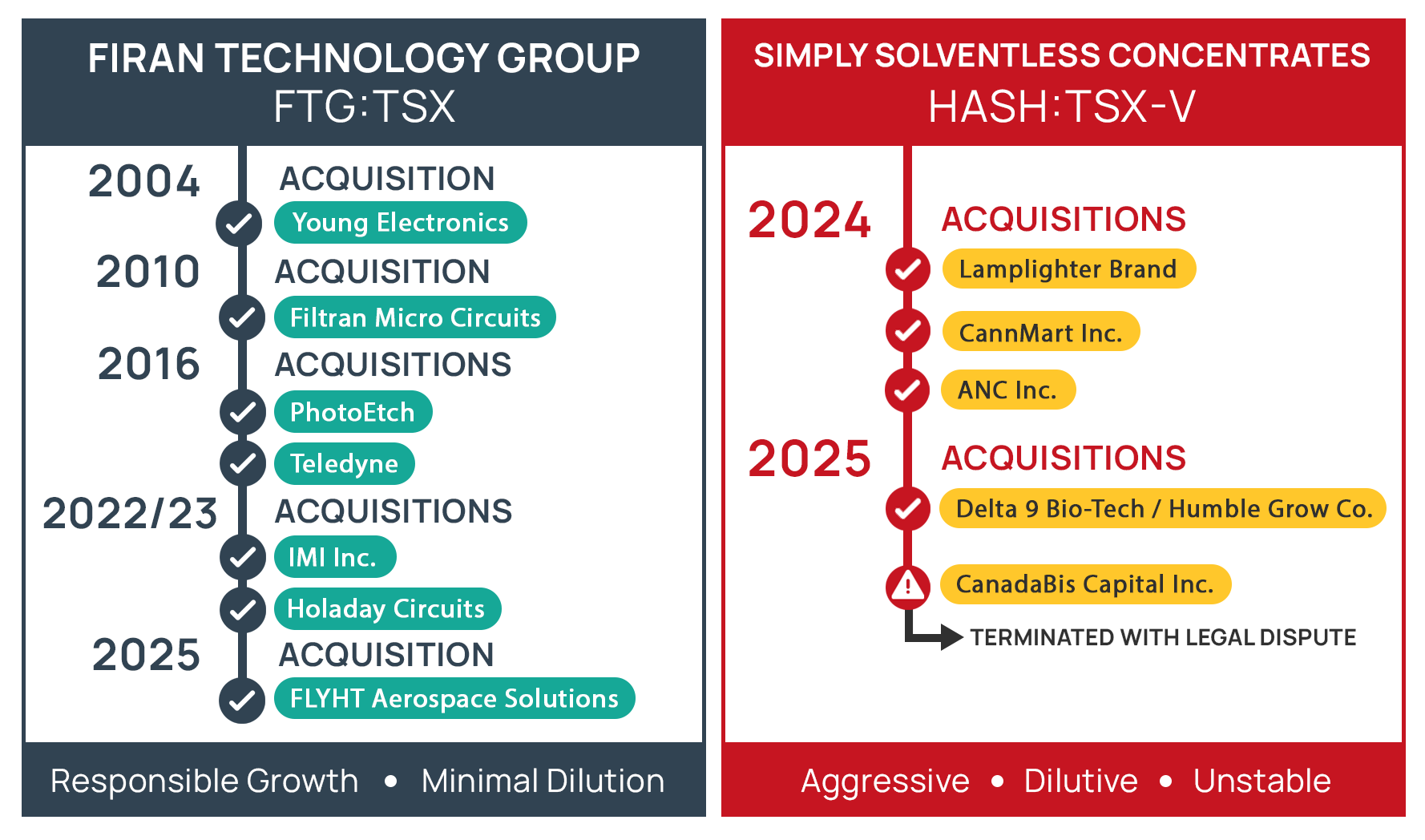

FTG’s Acquisition Timeline (Last 10 Years) – FTG also acquired Young Electronics & Filtran Micro Circuits in 2004 & 2010 respectively:

FTG’s growth journey reflects a patient and well-executed M&A strategy.

2016:

-

- PhotoEtch (Fort Worth, Texas): Acquired to expand customer base and product offerings. FTG successfully transitioned operations into existing facilities, closing the PhotoEtch site.

- Teledyne PCT (Hudson, New Hampshire): Similar to PhotoEtch, this acquisition aimed to expand product lines, with operations moved into FTG’s Chatsworth facility.

2022-2023:

Following the global shutdown of travel, a huge hit to aerospace, the business responsibly played defense and built a strong net cash balance sheet. Smartly, management leaned into the loosening of global restrictions, playing offense and buying two businesses primarily for cash on hand.

- IMI Inc. (IMI) (Haverhill, Massachusetts) – IMI is a manufacturer of specialty RF circuit boards focused on the aerospace and defense markets.

- Holaday Circuits (Minnesota-based) – added US manufacturing capacity for RF and high-technology products for aerospace and defense applications – combined sales of $45 million pre-pandemic.

Q1 2025:

-

- FLYHT Aerospace Solutions Ltd.: A significant acquisition enhancing FTG’s presence in the commercial aerospace aftermarket and expanding product offerings, particularly on Airbus aircraft. This deal reinforces FTG’s commitment to strategic, accretive growth in its core sectors.

Throughout these acquisitions, FTG has demonstrated a commitment to managing its debt effectively. For example, in its Q1 2025 results, even after the FLYHT acquisition and significant investments, FTG reported a healthy net debt of only $8.3 million. The company’s consistent generation of strong operating cash flow has been instrumental in its ability to take on debt for strategic growth and then deleverage.

FTG’s Minimal Share Dilution:

A hallmark of FTG’s responsible growth strategy is its commitment to limiting shareholder dilution. Over the past decade, despite multiple acquisitions, the company has largely avoided significant share issuances to fund these deals.

Weighted Average Shares Outstanding:

-

- FY 2016 (year of PhotoEtch & Teledyne PCT): Approximately 24.09 million shares.

- Q1 2025 (post-FLYHT acquisition): Approximately 24.92 million shares.

This represents an increase of less than 4% in shares outstanding over nearly a decade of significant growth and multiple acquisitions, demonstrating remarkable financial discipline and a strong focus on enhancing per-share value.

FTG’s Share Price Performance: A Testament to Responsible Growth

The long-term performance of FTG’s stock price directly reflects the success of its disciplined growth strategy. On May 15, 2015, KeyStone Financial recommended FTG as a buy at $1.35. Today, with the shares trading at $11.21, investors who followed that recommendation have seen substantial returns.

| Recommended | Recommended Price | Current Price | Industry |

|---|---|---|---|

| May 2015 | $1.35 | $11.21 | Aerospace & Defense Electronics |

This represents an approximate 733% gain over a decade, significantly outperforming North American market indices and showcasing the power of strategic, non-dilutive growth.

Year-to-date, the stock has increased 57.89%.

Access KeyStone’s Most Recent Update on Geodrill (GEO:TSX)

Updated GEO research report with full analysis of Q1 2025 results, new (BUY/SELL) rating, analysis, and fair value. Do not miss out!

![]()

Simply Solventless Concentrates (HASH): The Perils of Aggressive, Dilutive Growth

In stark contrast, Simply Solventless Concentrates Ltd. (HASH: TSX-V) provides a recent example of an aggressive growth-by-acquisition strategy that has heavily relied on share issuance, leading to significant dilution and adverse impacts on shareholder value. Operating in the rapidly evolving and often volatile cannabis sector, SSC embarked on a rapid acquisition spree over the past two years, aiming for swift market share gains.

SSC’s strategy has involved:

- Rapid Acquisition Pace: Quickly acquiring multiple entities in a short timeframe.

- Significant Share Issuance: A heavy reliance on issuing new equity to finance these acquisitions and related operations.

- Integration Challenges: Publicly reported delays and issues with financial filings, partly attributed to the complexities of integrating acquired entities.

SSC’s Acquisition Timeline (Last 2 Years):

SSC’s recent acquisition spree:

2024:

-

- Lamplighter brand.

- Licensed producer CannMart Inc.

- Pre-roll co-manufacturer ANC Inc.

Early 2025 (subsequent to Dec 31, 2024):

-

-

- Delta 9 Bio-Tech (rebranded to Humble Grow Co.).

- Proposed acquisition of CanadaBis Capital Inc. (later terminated, leading to a legal dispute).

-

SSC’s Significant Share Dilution:

The most striking difference in SSC’s strategy is the substantial increase in its outstanding share count. To finance its rapid expansion and operations, SSC has heavily relied on issuing new shares, dramatically diluting existing shareholders.

Approximate Share Count Evolution:

-

- Early aggressive M&A phase (start of 2024): SSC’s share count near the start of 2024 was ~38.69 million.

- Current (June 2025): Simply Solventless Concentrates has approximately ~108.6 million.

This represents an increase of ~181% in one and a half years in shares outstanding from the beginning of its aggressive acquisition period to today, largely driven by these acquisitions and related financing activities, including the settlement of debt with shares. This level of dilution means that even if the company’s overall value grows, the value per share can be significantly eroded. Essentially, it is difficult to post long-term per share growth.

SSC’s Share Price Performance: A Reflection of Dilution and Instability

The market’s reaction to SSC’s aggressive, dilutive strategy and operational challenges has been unfavorable, particularly in 2025.

SSC Share Price Year-to-Date 2025:

| January 2, 2025 | June 24, 2025 |

|---|---|

| $0.74 | $0.20 |

This translates to a significant 72.3% loss year-to-date in 2025, highlighting the severe consequences of a highly dilutive growth strategy combined with integration difficulties and financial uncertainties (such as audit delays and a management cease trade order). We also point out the companies press releases and presentations on our initial research included very interesting and aggressively positioned “proforma projected annualized revenue” & “proforma projected annualized normalized net income per share”. Certainly, figures we do not see quoted widely by management teams and at the very least we considered a very aggressive way to position the business to investors.

Conclusion: The Virtue of Patience and Prudence

Firan is run by a sharp, straight-shooting CEO who is patient, excellent operationally, but has been aggressive when opportunity presents itself. These are many of the qualities needed by a business that aims to complement organic growth with strategic growth-by-acquisition. Simply Solventless appears to be run by finance guys, who expanded via aggressive dilutive share issuances with little patience, a lack of execution, and a good deal of unrealistic forward-looking numbers. One small cap business we have recommended and owned for a decade, the other we took a hard pass on.

The contrasting trajectories of Firan and Simply Solventless Concentrates serve as a powerful lesson for companies eyeing growth by acquisition. While the allure of rapid expansion is strong, the responsible and measured approach championed by FTG – characterized by strategic acquisitions, disciplined debt management, and minimal shareholder dilution – has clearly led to superior near and long-term shareholder returns.

Conversely, SSC’s aggressive, highly dilutive strategy, though perhaps aiming for swift market share gains, has resulted in substantial shareholder value destruction. The market ultimately rewards sustainable, well-integrated growth that builds intrinsic value per share, rather than simply expanding through the issuance of a flood of new shares. For investors, these case studies underline the critical importance of scrutinizing a company’s financing methods and integration capabilities when evaluating M&A-driven growth strategies.

Investing is as much about avoiding the wrong stocks as it is finding the right ones. We help our clients do both. Don’t gamble on hype — get the research advantage with KeyStone.