The Mining Money Trail: Junior Mining Financing Heats Up in 2025

Despite a backdrop of relatively strong commodity prices, the junior and intermediate mining sector experienced a significant capital drought in 2024, only to stage a potentially sustainable rebound in 2025. This surge in junior mining financings suggest a renewed appetite for risk and growth capital, with major implications for the sector’s service providers.

The 2024 Slump: A Five-Year Low

2024 proved challenging for Junior and Intermediate mining companies raising capital. According to data tracked by S&P Global, funds raised by junior and intermediate mining companies fell by 12% to US$10.27 billion, marking its lowest level in five years. This slowdown occurred despite inflation-fueled commodity strength and a 2% increase in the total number of transactions, indicating smaller deal sizes and cautious investor sentiment.

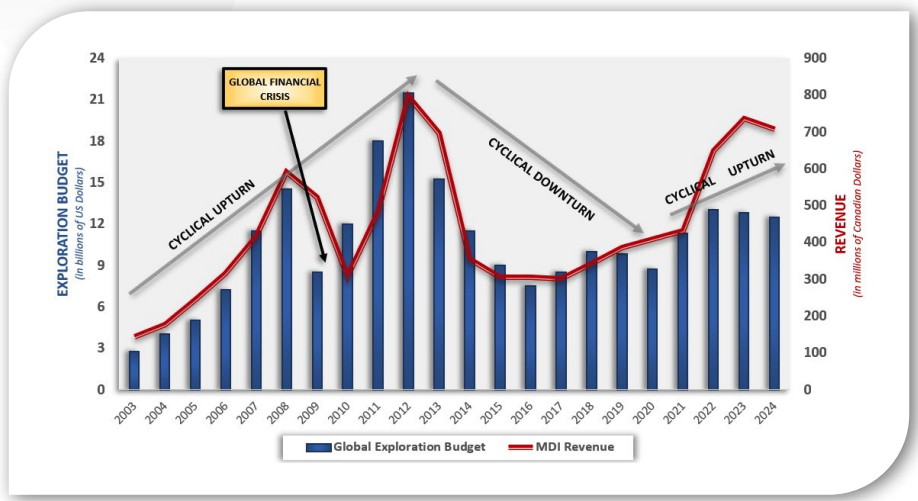

Global exploration budgets reflected this wariness, with nonferrous metals exploration totaling an estimated US$12.5 billion in 2024 – a decline of approximately 3% from 2023. This dip was characterized by an 8% and 5% decrease in grassroots and late-stage exploration budgets, respectively, contrasting with a 2% increase in mine site exploration, suggesting capital was prioritized for known assets rather than frontier discovery.

The 2025 Pivot: Financing Momentum Increasing

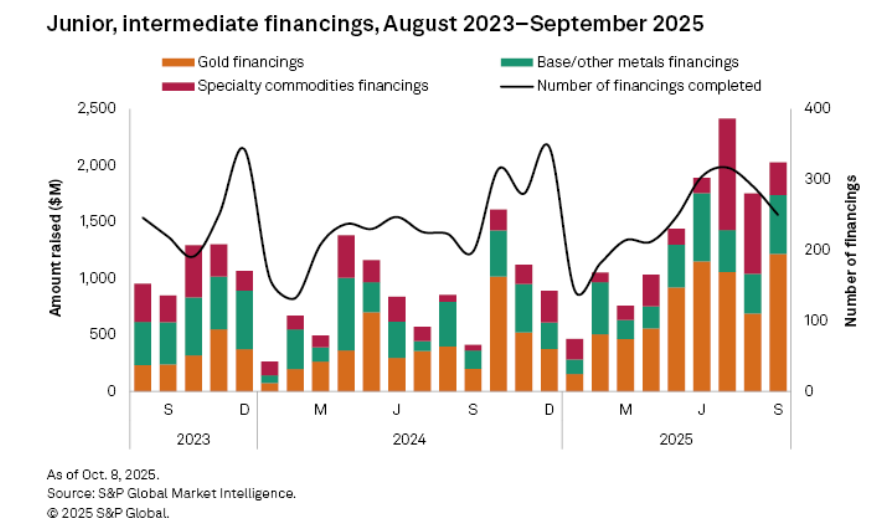

Fast forward to today, the narrative has shifted from the lows of 2024. Fuelled by continued strong commodity prices, including the record price of gold above US$4,000/oz, access to capital appears to be improving. According to S&P Global data as of October 2025, Year-to-Date (YTD) funds raised by Junior and Intermediate Mining Companies have already reached US$12.8 billion, exceeding the full-year 2024 total of US$10.3 billion. YTD gold financings rebounded sharply, rising 136% year over year to US$6.7 billion, reaching a new all-time record month in September of $1.2 Billion (dating back to January 2014).

Source: S&P Global Market Intelligence October 2025 Funds Raised

This resurgence is evident on major markets like the TSX and TSX-V. During the first eight months of 2025, mining companies listed on these exchanges completed 837 financings (up from 794 in 2024) and raised C$6.4 billion of equity capital, according to TMX Money. While this is less than the C$7.9 billion raised in the comparable 2024 period, the 2024 figure included an outsized C$1.6 billion equity offering by First Quantum Minerals Ltd for the restructuring of the Cobre Panama Copper mine. A more telling comparison shows 2025’s C$6.4 billion is a significant increase over the C$5.1 billion raised across 818 financings in the first eight months of 2023, confirming a potential growth trend.

Despite the strength in financing, the spending outlook remains moderated, with S&P anticipating that global exploration budgets for 2025 will likely follow “a similar track” to 2024’s US$12.5 billion.

Source: Major Drilling (MDI:TSX) October 2025 Investor Presentation

Will This Junior Financing Strength Lead to Significant Tailwinds for Commodity Service Companies?

The capital raised by junior and intermediate miners is their lifeblood, primarily dedicated to advancing projects through various stages – from initial exploration to feasibility studies and, ultimately, development. As such, the strength in financing is promising and could lead to a tailwind for the sector.

Two of KeyStone’s exclusive recommendations for clients service the mining sector. The first, up 84% in just 10 months from its initial recommendation to clients, while the second is up over 120% in 5 years from our initial recommendation. Both have the potential for even more gains if demand from junior mining companies increases!

The mechanism for the tailwind, capital deployment: Injection of fresh capital must eventually be spent to create value. This money directly flows to the service sector, including:

-

Drilling Companies: To support increased exploration and resource definition activities.

Example: Major Drilling (MDI:TSX), the world’s largest mineral driller operating in over 20 countries around the world with 709 Drills at Q1 2026, with capacity utilization of 50%. Although we like other drillers in the space due to their higher risk-to-reward investment thesis, the business maintains a relatively healthy balance sheet and could benefit from a sustainable rebound in junior financings.

View my recent take of MDI on KeyStone’s podcast here.

-

Engineering Firms: For preliminary economic assessments (PEAs), pre-feasibility, and feasibility studies.

Example: Eagle Plains Resources Ltd. (EPL:TSX-V) is not a pure play engineering firm for the mining sector, as it owns interests in several mineral exploration projects. But effectively 100% of its revenue comes from its subsidiary, Terralogic Exploration, a Geological Contractor providing geological mapping, geophysical surveys, drill programs, project design and budgeting, geologic modelling, resource calculation, and permitting. While Eagle Plains is not a business that meets our investment criteria due to its lack of profitability, its core revenue generating business could benefit from increased activity.

-

Equipment and Logistics Providers: As projects advance toward mine-site construction and operation.

Example: Toromont Industries Ltd. (TIH:TSX), rents and sells heavy duty equipment to the road building, mining, infrastructure, residential & commercial construction, power generation, forestry, agriculture, and waste management markets. While the business currently trades above its historical median P/E multiple of 20 times, it maintains a robust balance sheet with $83M in net cash, a 1.3% dividend yield that has grown 11% over the past 5 years, all while the business compounded EPS at 14% from 2015-2024. Toromont could benefit from increased exploration activity, in fact, Toromont Cat, a subsidiary of Toromont Industries, helped supply the first autonomous mine in North America: Cote Gold Mine, Ontario.

In essence, the service sector acts as the primary recipient of capital expenditure within the mining industry. There is no guarantee that the recent strength in junior mining financings will lead to a sustainable increase in activity into 2026 – and a time lag of at least 6 months before a boost to demand is expected – but those willing to bet on a sustainable increase could be handsomely rewarded into 2026/27.

At KeyStone Financial, we cut through the noise of the markets to uncover high-quality, under-the-radar growth and income stocks — including unique opportunities positioned to benefit from trends like the resurgence in Junior Mining Financing. Become a KeyStone client today and gain immediate access to our latest BUY recommendations, exclusive reports, and actionable insights designed to help you build a winning stock portfolio.