You are listening to KeyStone’s Stock Talk Podcast – Episode 303

Great to chat with you again. We kick off the festivities with Part 2 of an article I authored this past week on a tale of two Small Cap M&A Stock Strategies – comparing the successful, measured approach of KeyStone recommendation Firan Technology (FTG: TSX) which has gained 700+ percent vs. the aggressive, equity diluting strategy of a company we passed Simply Solventless (HASH: TSX-V), which, well, has not. In our YSOT segment Brennan looks at Kraken Robotics Inc. (PNG:TSX-V), a marine technology company, which produces optical sensors, batteries, and underwater robotic equipment for unmanned underwater vehicles (UUVs) used in military and commercial applications (80% defence / 20% commercial). The small cap, closed a $115 Million Bought Deal Public Offering this week and Brennan let’s you know how Kraken plans to put the funds to use. Aaron answers a viewer question on OR Royalties Inc. (OR: TSX), an intermediate precious metal royalty and streaming company, which has seen its share price surge 60% in 2025. Aaron will explain why. Finally, in our Star & Dog Segment, Brett starts with our Dog of the Week, Simulations Plus, Inc. (SLP:NASDAQ), which provides modeling and simulation software and consulting services primarily for the pharmaceutical and biotechnology industries. The stock is down 70% over the past year, with the most recent losses coming after the company dropped Q3 earnings expectations. Our Star of the Week is MP Materials Corp. (MP:NYSE), a rare earth element company which has seen its shares increase 91% over the last month, with 85% of the increase coming over the past week. Brett let’s you know why.

Let’s get to the show – I welcome my cohost, Mr. Aaron Dunn, and the killer B’s, Brett and Brennan.

Firan Technology (FTG: TSX) vs. Simply Solventless (HASH: TSX-V) – A Tale of Two Small-Cap M&A Stock Strategies

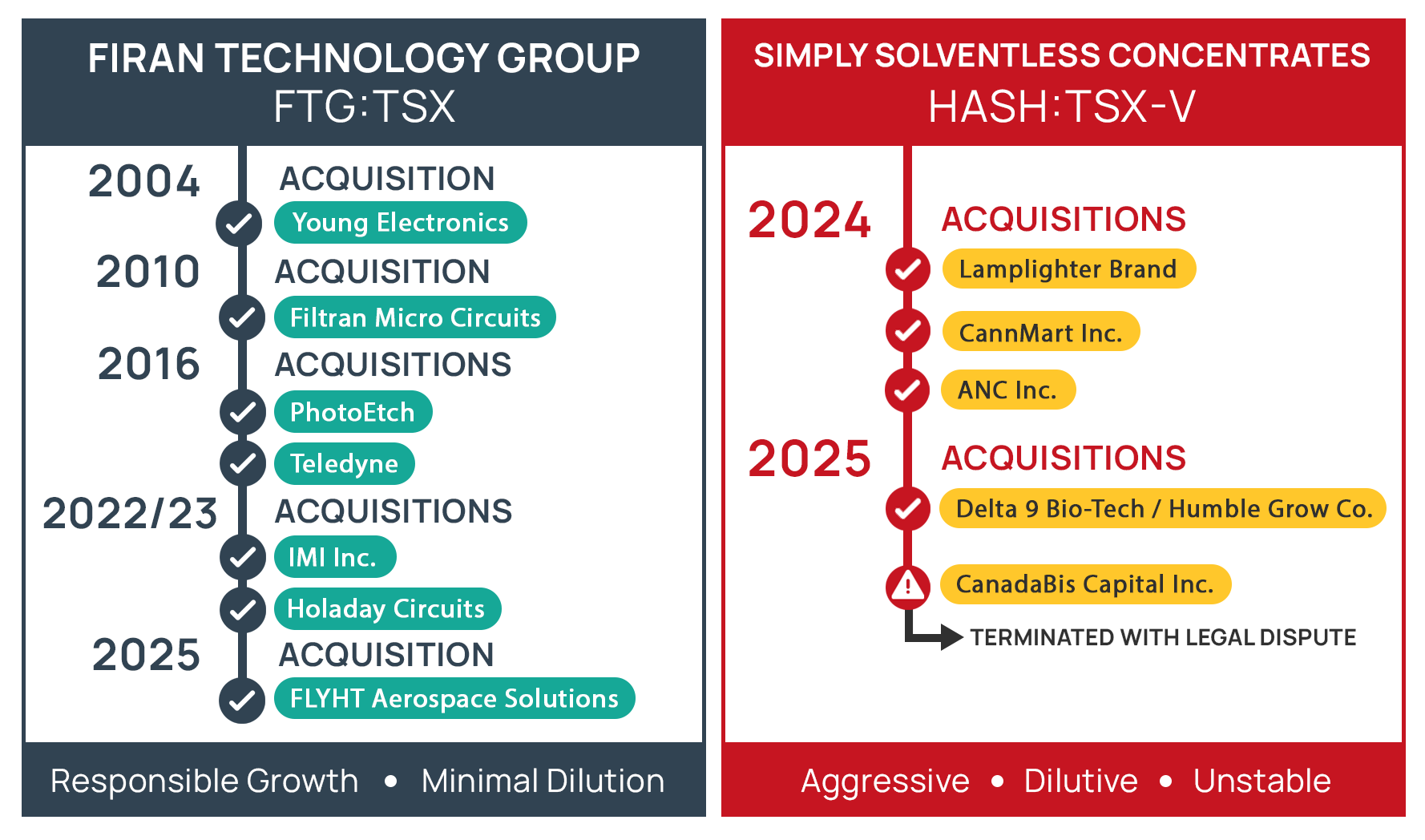

This segment juxtaposes the responsible acquisition strategy of Firan Technology Group Corporation (TSX: FTG) with the more recent aggressive, dilutive approach of Simply Solventless Concentrates Ltd. (TSX-V: HASH), illustrating how their respective paths have impacted shareholder returns. We have interviewed management at both small cap companies. One we have recommended and owned for a decade, the other we took a hard pass on.

Businesses that use a “M&A” as their primary growth driver walk a fine line. For every massive success story like the Boyd Group, a serial acquirer of auto repair shops recommended by KeyStone in 2008 at $2.30 which today trades above $200.00, there are ten Dye & Durham’s (DND: TSX) or Lightspeed Commerce’s (LSPD: TSX) – decent business that executed poorly on an aggressive growth-by-acquisition strategy. The are also countless roll up “stories” that niver even get out of the starting gate and end up destroying investor capital.

Unfortunately, the microcap market is also littered with failed or failing M&A strategies, including a recent example which I will touch on next week in Part 2 – Simply Solventless Concentrates Ltd. (HASH: TSX-V), the company provides an excellent foil for the more measured and successful M&A strategy of Firan Technology Group Corporation (FTG:TSX).

Growth-by-acquisition in reality.

While sexy in theory, growth-by-acquisitions can be a risky strategy, with many high-profile examples of mergers and acquisitions failing, often spectacularly. The reality is, a significant number of acquisitions fail to meet expectations, with estimates ranging from 70% to 90%. Common reasons for failure include poor integration, overpaying for the target company, overestimated synergies, cultural clashes, and a lack of strategic alignment.

KeyStone’s preferred growth strategy. A mix of measured M&A funded by cash flow, cash on hand, or reasonable debt. Always with an eye towards continued organic growth. Last show I provided an example from KeyStone’s Canadian Small-Cap Research of an affective M&A strategy – in Firan Technology Group Corporation (FTG:TSX). This week, we present the foil for Firan’s successful strategy, Simply Solventless Concentrates (HASH:TSX-V) and show the The Perils of Aggressive, Dilutive Growth.

The business: Simply Solventless is a Canadian cannabis company that specializes in the cultivation, processing, formulation, and sale of terpene-rich solventless cannabis concentrates.

M&A strategy: In stark contrast to Firan, Simply Solventless Concentrates Ltd. (HASH: TSX-V) provides a recent example of an aggressive growth-by-acquisition strategy that has heavily relied on share issuance, leading to significant dilution and adverse impacts on shareholder value.

Operating in the rapidly evolving and often volatile cannabis sector, SSC embarked on a rapid acquisition spree over the past two years, aiming for swift market share gains. SSC’s strategy has involved:

- Rapid Acquisition Pace: Quickly acquiring multiple entities in a short timeframe.

- Significant Share Issuance: A heavy reliance on issuing new equity to finance these acquisitions and related operations.

- Integration Challenges: Publicly reported delays and issues with financial filings, partly attributed to the complexities of integrating acquired entities.

SSC’s Acquisition Timeline (Last 2 Years):

In 2024, the company acquired the Lamplighter brand.

- Licensed producer CannMart Inc.

- Pre-roll co-manufacturer ANC Inc.

Early 2025

Delta 9 Bio-Tech (rebranded to Humble Grow Co.). and made a…..

- Proposed acquisition of CanadaBis Capital Inc. (later terminated, leading to a legal dispute).

SSC’s Significant Share Dilution:

The most striking difference in SSC’s strategy is the substantial increase in its outstanding share count. To finance its rapid expansion and operations, SSC has heavily relied on issuing new shares, dramatically diluting existing shareholders.

Approximate Share Count Evolution:

- Early aggressive M&A phase (start of 2024): SSC’s share count near the start of 2024 was ~38.69 million.

- Current (June/July 2025): Simply Solventless Concentrates has approximately ~108.6 million.

This represents an increase of ~181% in one and a half years in shares outstanding from the beginning of its aggressive acquisition period to today, largely driven by these acquisitions and related financing activities, including the settlement of debt with shares. This level of dilution means that even if the company’s overall value grows, the value per share can be significantly eroded. Essentially, it is difficult to post long-term per share growth.

SSC’s Share Price Performance: A Reflection of Dilution and Instability

The market’s reaction to SSC’s aggressive, dilutive strategy and operational challenges has been unfavorable, particularly in 2025.

This translates to a significant 69.23% loss year-to-date in 2025, highlighting the severe consequences of a highly dilutive growth strategy combined with integration difficulties and financial uncertainties (such as audit delays and a management cease trade order). We also noted the companies press releases and presentations on our initial research included very interesting and aggressively positioned “proforma projected annualized revenue” & “proforma projected annualized normalized net income per share”. Certainly, figures we do not see quoted widely by management teams and at the very least we considered a very aggressive way to position the business to investors.

Conclusion: The Virtue of Patience and Prudence

Firan is run by a sharp, straight-shooting CEO who is patient, excellent operationally, but has been aggressive when opportunity presents itself. These are many of the qualities needed by a business that aims to complement organic growth with strategic growth-by-acquisition.

Simply Solventless appears to be run by finance guys, who expanded via aggressive dilutive share issuances with little patience, a lack of execution, and a good deal of unrealistic forward-looking numbers.

One small cap business we have recommended and owned for a decade, the other we took a hard pass on.

The contrasting trajectories of Firan and Simply Solventless Concentrates serve as a powerful lesson for companies eyeing growth by acquisition. While the allure of rapid expansion is strong, the responsible and measured approach championed by FTG – characterized by strategic acquisitions, disciplined debt management, and minimal shareholder dilution – has clearly led to superior near and long-term shareholder returns.

Conversely, SSC’s aggressive, highly dilutive strategy, though perhaps aiming for swift market share gains, has resulted in substantial shareholder value destruction. The market ultimately rewards sustainable, well-integrated growth that builds intrinsic value per share, rather than simply expanding through the issuance of a flood of new shares. For investors, these case studies underline the critical importance of scrutinizing a company’s financing methods and integration capabilities when evaluating M&A-driven growth strategies.

Investing is as much about avoiding the wrong stocks as it is finding the right ones.

Kraken Robotics Inc. (PNG:TSX-V) – Viewer Request

| COMPANY DATA | |

| Symbol | PNG:TSX-V |

| Stock Price | $3.38 |

| Market Cap | $1.0 B |

| Dividend Yield | N/A |

This question comes in from Glen via email, as well as our client Bryan, who asked me about the stock just the other day.

Kraken is a marine technology company, which produces optical sensors, batteries, and underwater robotic equipment for unmanned underwater vehicles (UUVs) used in military and commercial applications (80% defence / 20% commercial).

The company is based in St. John’s Newfoundland and has operations throughout North America and internationally, with approximately 2/3rds of revenue coming from North America over the last 2 fiscal years…

And it operates in two segments, Products, and Services (with over 2/3 coming from the products segment).

The stock has performed very strong over the past 3 years, up over 750% since late 2022, and up about 190% over the past year.

We have interviewed Kraken’s management of the company in the past and covered the business on the podcast a few times now. With Aaron covering them back in the Summer of 2023 and 2024, and Ryan covering them more recently in the spring of 2025.

And over this time we have seen them go from a money losing business, which has transitioned into more consistent net profit. So lets take a look at where they are today under the scope of our Growth at a Reasonable Price (or GARP) investing criteria.

Just to go over some operational updates here:

On July 7th, 2025, the company announced that it had closed it previously announced bought deal, issuing 43.2M common shares at a price if $2.66 per share for gross proceeds of $115M. With the proceeds expected to be used for enhancing its balance sheet for acquisitions, working capital for larger potential contracts, and general corporate purposes. This will now place the company’s outstanding share balance to over 300 million, and as you can see on the right hand side of the screen, the company is not afraid of dilution, issuing over 150 million shares over the last 5 years.

And the company has consistently been bringing in contracts, and as Ryan discussed in our last segment clarified details around its new Halifax-based battery manufacturing facility which is expected to cost $10M to construct and will be operation by Q4 2025 and is estimated to produce up to $200M in annual revenue at full capacity.

The company has also made acquisitions such as its deal of “3D at Depth” for US$17M, which reported revenue of US$14M and operating income of US$1.1M in FY 2024. Or partnerships like it has established with SeeByte to enhance their complimentary system offerings and their Cooperative Research and Development Agreement (CRADA) with Naval Undersea Warfare Center Division, Newport (NUWCDIVNPT) to advanced signal processing techniques for the current and future generation of Synthetic Aperture Sonar (SAS) sensor technologies.

One thing I will note though, is the company does not report a backlog figure.

So let’s look at the financials for Q1 2025 ended March 31, 2025:

- Revenue was down 23% to $16.1 million, with growth of 38% in its services segment, while its product revenue declined 42% due to lower revenues related to the RMDS program. Note though that this is a contract driven business and y/y quarterly variations can be quite volatile.

- Gross profit margin was 62.7% compared to 44.8% for the same period last year, with the increase related to higher margin projects in the quarter compared to the same period last year.

- Net Income was $250 thousand or $NIL on a per share basis, compared to a gain of $2.1 million or $0.01 per share in Q1 2024.

- The company posted Adjusted EBITDA of $2.8 million which was down 32% from the same period last year.

- With the decline in profitability due primarily to a decline in revenue as well as an increase in administration costs.

And I will also note that there was a large deferred tax recovery in Q4 2024 which inflated earnings, and when we get to my valuation section in the coming slides I do adjust this out.

Balance Sheet:

The balance sheet remains relatively healthy with net debt of $59.3M, with debt and leases of $30.5M, providing a net cash position of $28.7M or $1.48 per share. NOW keep in mind, the next quarter of Q2 2025 which will be for the period ending June 30, 2025, will not include its recent cash raised through the equity raise, but by Q3 2025 this will begin showing on the balance sheet. As well as the 300 million shares as a new denominator for its shares outstanding.

Outlook:

Looking toward FY 2025, management expects revenue of $120-$135 million, which represents growth of approximately 40% over FY 2024 and EBITDA of $26-$34 million, which

And adj. EBITDA is now expected to be in the lower end of its $24-$29 million range (due to tariffs), but at the midpoint represents growth of approximately 52% over FY 2025.

And looking at the valuation, this places the company at a pro-forma EV/Adj. EBITDA multiple of 22x (which takes into account its recent equity raise), and trades with a trailing EV/Adj. EBITDA of 44x and a trailing price-to-adj. earnings multiple of 99x (which all I am adjusting out from earnings is FX changes and deferred tax recovery, which it had a tax recovery of $8.6M in Q4 2024 which boosted reported earnings).

Conclusion:

Kraken is a fundamentally strong business which checks off several boxes from our GARP investment criteria, including:

-

- Good historical growth

- Strong backlog – new orders coming in (does not disclose backlog)

- Runway of growth and new capacity coming online

- Strong net cash balance sheet

- Some negatives though are that the company is not scared of dilution, and despite strong revenue and net income growth, the business was only able to grow Adj. EPS at 13% in FY 2024 (over FY 2023) when Adj. Net Income was up 23%. The caveat is that it is likely a good thing that the company is raising capital at these valuations.

- The valuation remains pricey at this point, with a pro-forma forward EV/Adj. EBITDA multiple of 22x. The growth is strong, but for it to continue to maintain this valuation, growth must be upheld which is a risk in a lumpy contract driven business.

- Global Defence spending is a tailwind for the business, but tariffs pose a risk.

Simulations Plus, Inc. (SLP:NASDAQ) – Dog of the Week

Simulations Plus, symbol SLP on the NASDAQ, has fallen dramatically over the past year, with a sharp decline after fiscal Q3 earnings. The stock is down 70% over the past year, with a 26% drop the day after fiscal Q3 earnings, trading at $12.97 a share a $261 million market cap.

Simulations Plus is a leading provider of cheminformatics, biosimulation, simulation-enabled performance and intelligence solutions, and medical communications to the biopharma industry. In addition to software sales, the company also offers consulting services. The revenue split was 60% software, 40% services for the year-to-date.

So why has the stock dropped so much?

First, let’s go back to June 11th, the shares dropped significantly as the company announced a lower guidance for Fiscal 2025 and preliminary revenue for Q3.

For Q3, the company announced preliminary revenue of $19 to $20 million.

And for 2025, revenue guidance was cut to $76 to $80 million from the prior guidance of $90 to $93 million.

The stock fell 24.6% by the close of the following day.

Now moving forward to Q3 earnings in full.

Revenue actually came in above the preliminary expectations at $20.4 million, 10% growth, including $2.4 million from the acquired Pro-ficiency; without it, organic revenue declined by 4%.

The top line growth was driven by a 17% increase in Medical Communication Services, but other service areas declined, with management attributing the decline to cautious spending behaviour, project delays or cancellations from Biopharma Clients. Which can be further attributed to market uncertainty around future spending, drug pricing and tariffs.

Gross profit came in at $13.0 million, a margin of 64%.

However, the company came in at a significant net loss of $67.4 million, $3.35 a share, due to a one-time non-cash impairment charge of $77.2 million to align book-value with the actual market-value. A massive impairment given that it is in the range of the fiscal 2025 guided revenue. The impairment was primarily due to the underperformance of forecasted revenue for the Adaptive Learning & Insights, ALI and Medical Communications, MC business units. Meaning weaker revenue will likely occur

And I will end this on a brighter note on April 10th, the FDA announced the phasing out of animal testing requirements, adopting AI methods which does benefit SLP.

However, for now Simulations Plus is our Dog of the Week!

MP Materials Corp. (MP:NYSE) – Star of the Week

The rare earth element company MP Materials, symbol MP on the NYSE, surged in price this week. The stock is up a whopping 91% over the last month, with 85% of the increase coming over the past week. The shares are now trading at $58.22, with a $9.5 billion market cap.

The company is the only integrated rare earth producer in the US, spanning from mining to magnets. Rare earth products are used across industries, transportation, energy, robotics, defence and aerospace.

KeyStone highlighted the company back in 2023, at the time the company was facing lower rare earth prices and was ongoing Stage 2 of 3 of its strategic plan.

A quick outline of the plan:

- Stage I The production of rare earth ore at the Mountain Pass Mine

- Stage II Separation of rare earth elements

- Stage III production of rare earth metals, alloys, and permanent magnets

The company commenced the production of neodymium-praseodymium (NdPr) metal and trial production of automotive-grade magnets in January of this year at its Fort Worth, Texas, facility.

While the progress of its strategic plan is obviously a plus, it was not the catalyst behind the surge in price.

In Trump’s tariff spat with China back in April, China cut off the supply of rare earth magnets to the US on April. China represents over 60% of the rare earth ore mined and processes over 90%. This put pressure on US automakers and the US defence industry. Although rare earth magnets aren’t overly expensive, the complete loss of the magnets makes the end product, whether a car or a fighter jet, impossible to manufacture.

Leading us to just last week, on July 10th, the US Department of Defence, DoD, announced a $400 million direct investment in MP in convertible preferred stock and warrants, which will have the DoD becoming the largest shareholder at 15% of shares, if fully converted.

In part of the agreement, MP is looking to build its second domestic magnet facility “10x” by 2028 with expected production of 10,000 tons. JPMorgan and Goldman Sachs are set to finance a further $1.0 billion for the facility. Further, the DoD will provide a $150 million loan to expand the company’s heavy earth element separation capabilities at Mountain Pass.

And perhaps one of the most interesting aspects of this deal is that the DoD is creating a price-floor commitment at $110/kg of products sold or stockpiled. This is a significant factor as it lowers the downside of production, over-doubling the $52/kg in Q1. Rare earth metals and products go through significant price swings, so a floor is necessary to ensure profitability – This will cost the DoD and thus the US tax payer but it does ensure constant production of NdPr magnets regardless of economic conditions.

Next MP had another huge announcement on Tuesday, the 15th.

The company announced a $500 million partnership with Apple to Produce Recycled rare-earth magnets in the United States

MP will construct a commercial-scale recycling line at Mountain Pass for magnet scraps and components from end-of-life products. MP will also expand its Fort Worth magnet facility to meet demand.

After two massive announcements, MP Materials is our Star of the Week!