You are listening to KeyStone’s Stock Talk Podcast – Episode 305

This week, I will kick off our YSOT segment answering a viewer question on 5N Plus (VNP: TSX), a global producer of specialty semiconductors and performance materials. Powered by record quarterly profitability, the stock is up over 50% in the past month – we revisit the company and let you know what is driving the growth. Second, Brett takes a look at Cipher Pharmaceuticals (CPH: TSX), a small-cap Canadian Pharma company that clients should be familiar with. KeyStone recommended the company at $3.89 a share back in August of 2023, just under 2 years ago and today it trades above $15, up nearly 300%. After a very strong quarter, Brett let’s you know where this small-cap start is at. Brennan takes a viewer question on, The Honest Company (HNST: NASDAQ) – Jessica Alba’s personal care company dedicated to creating clean-and sustainably designed products. Brennan takes his third look at the business and let’s you know if Alba shines as brightly in the markets as she does on screen. Finally, Aaron gives his take on the recent Q2 report from Amazon.com Inc. (AMZN: NASDAQ).

Let’s get to the show – I welcome my cohost, Mr. Aaron Dunn, and the killer B’s, Brett and Brennan.

Poll Question

YSOT 5N Plus Inc. (VNP: TSX) – Viewer Request

| COMPANY DATA | |

| Symbol | VNP: TSX |

| Stock Price | $15.09 |

| Market Cap | $1.343B |

| Dividend Yield | N/A |

I reviewed 5N Plus earlier in the year when the stock was up 62% year to date. With VNP now up over 90% year-to-date, and 53% in the last month, we are fielding more questions and I will revisit.

5N Plus is global producer of specialty semiconductors and performance materials. They focus on developing and manufacturing advanced materials that are essential components for a wide range of products in critical industries.

Here’s a breakdown of their business:

- In Specialty Semiconductors: 5N Plus produces ultra-high purity metals and compounds, often with “five nines” (99.999%) purity or more (thus the “5N” in their name). These materials are crucial for applications in:

- Terrestrial Renewable Energy: They are a major supplier of materials like cadmium telluride (CdTe) for thin-film solar modules, which convert sunlight into electricity.

- Space Solar Power: They develop and manufacture multi-junction solar cells for satellites and spacecraft, powering critical space missions.

- Imaging and Sensing: Their materials are used in radiation detectors for medical imaging (e.g., X-rays, gamma rays), security, and defense applications.

- Performance Materials: This segment focuses on materials that enhance the performance of various products, including:

- Health and Pharmaceutical: They produce bismuth-based Active Pharmaceutical Ingredients (APIs) for over-the-counter medications (like antacids), antibiotic creams, and other human care products.

- Technical Materials: This includes things like low melting point alloys (used in aviation and other industries) and various bismuth chemicals that serve as lead replacements in different industrial applications (coatings, pigments, electronics).

So what is driving the share price gains – a couple of items announced over the past 10 days.

- 5N Plus siged a scaled up and expanded critical materials supply agreement with first solar – we will delve further into this shortly.

- Strong Q2 numbers and increased annual guidance.

Q2 2025 Financial Snapshot:

Revenue in Q2 2025 increased by 28% to $95.3 million, compared to $74.6 million in Q2 2024. The increase is primarily attributable to higher sales in the terrestrial renewable energy and space solar power sectors under Specialty Semiconductors, and higher bismuth-based product pricing under Performance Materials.

Adjusted EBITDA in Q2 2025 increased by 79% to $24.1 million, compared to $13.5 million in Q2 2024, driven by higher volumes in the terrestrial renewable energy and space solar power sectors, and better prices over inflation for both solar power and bismuth-based products.

Adjusted gross margin as a percentage of sales was 34.6% in Q2 2025, compared to 31.3% in Q2 2024., favourably impacted by the same factors as above.

Net earnings in Q2 2025 were $15.2 million or $0.17 per share, compared to $4.8 million or $0.05 per share in Q2 2024.

First Solar deal:

- Volume commitments for the contract underway increased by 33% (2025 to 2026).

- Volumes in the following periods (2027 to 2028) also rose 25%.

- Commentary suggests that almost all supply is going into the US market under favourable pricing /margins.

- Capex to expand capacity is minimal given there are no changes needed at the exiting facilities (same footprint in Montreal with additional reactors added)

- 5N Plus also further entrenched its relationship with First Solar by starting to supply cadmium selenide (CdSe) – in the simplest terms it is an additive layer to new thin film solar cells that improves efficiency and performance – this is not a large or needle moving part of the agreement.

Outlook & Guidance:

Through the second half of 2025, 5N+ anticipates demand under Specialty Semiconductors from the terrestrial renewable energy and space solar power markets to accelerate, as customers look to secure advanced materials from trusted and reliable partners. Under Performance Materials, consistent with historical trends, volumes through the second half of 2025 are expected to be slightly lower than compared to the first half of 2025, with margins continuing to benefit from the Company’s strategic global footprint and sourcing capabilities in the current volatile business environment.

Based on its financial performance year to date, coupled with anticipated demand under Specialty Semiconductors and better than anticipated performance under Performance Materials, Adjusted EBITDA guidance for 2025 has been revised upwards from a range of $55 to $60 million, last updated on February 25, 2025, to a range of $65 to $70 million.

Looking ahead, the Company stated it will will continue to remain prudent in an evolving geopolitical environment, including with regards to its impact on operating costs. Management stated, 5N+ is well-positioned to continue solidifying its leadership in key end markets through the end of 2025 and going into 2026.

Valuations:

- 2025e EV/EBITDA: ~13.1x.

- 2025e P/Aeps: ~24.4x.

- 2026e EV/EBITDA: ~11.3x.

- 2026e P/Aeps: ~21.8x.

Conclusion:

5N Plus is a critical Western supplier of specialty semiconductors and performance materials for the solar, extra-terrestrial energy, and medical imaging / bismuth API markets. Its products are essential to each vertical, and it appears from customer behavior around recent contract extensions and incremental spot demand that VNP may have a solid moat.

Trailing valuations are on the higher end, but if growth projections for 25% compounding for the next decade are correct, the stock could be attractive – we expect quarterly lumpiness.

Monitor – strong Q2 numbers and strong outlook.

YSOT The Honest Company (HNST:NASDAQ) – Viewer Request

| COMPANY DATA | |

| Symbol | HNST:NASDAQ |

| Stock Price | $4.03 |

| Market Cap | $416M |

| Dividend Yield | N/A |

The Honest Company is a personal care company dedicated to creating clean-and sustainably-designed products. Its products include baby clothing, diapers, wipes, nursery products, skin-care, and makeup.

The company was co-founded by actress Jessica Alba and IPO’d at $16 per share in 2021 raising over $400 million.

We have covered the stock a few times on the podcast now, the first time was back in November 2024 following the company’s solid Q3 2024 results when the stock was trading in the $7.30 range. And the second time was just a couple of months ago in May of 2025 while the stock was trading around $5.40 per share.

And we have been getting quite a few questions on the business, and actually right before its Q2 results, the stock had a volatile day with one of our Youtube watchers stating “What happened with HNST today! Rug pull”…… despite the stock being down just 3%.

Now I must say, if you are using the definition “rug pull” to describe a 3% decline in the price of a stock… you clearly do not know what you are talking about… As for those who do not know, a “rug pull” is a type of scam in the cryptocurrency space where developers abandon a project taking investor funds with them… essentially causing the price of the cryptocurrency to plummet and investors left holding the bag….. so personally, I would not use the Honest Corp & Rug Pull in the same sentence… But anyways, the company reported its Q2 results last week on August 6th, so lets dig into the business to see how it is looking today and whether it looks like a “steal of a deal” like Andy (one of our other youtube listeners indicated).

When we looked at the long-term financials in November 2024, the business’s revenue was growing with a CAGR of ~10% (since 2019), but profitability was lacking. Although it was trending in the right direction. And the same thing could be said after I reviewed the Q1 2025 results, revenue growth was good, and the company had reported its 6th consecutive quarter of positive EBITDA.

Now looking at Q2 2025:

- Revenue was up only 0.4% to $93M and was driven by an increase in retail revenue but partially offset by a decline in Honest.com revenue. With management indicating that in Q2, shipments trailed consumption partially offsetting the first quarter of 2025 results where shipments were ahead of consumption by 5%.

- Gross margin increase 210 basis points to 40.4% driven by a change in inventory reserves, partially offset by tariff costs..

- But I will note that as part to mitigate the impact of tariffs, the company increased inventory on hand during the first half of 2025.. but there was a bit of tariff impact in the quarter and it has come sooner than management has anticipated.

- Adjusted EBITDA was positive $7.6 million compared to $7.6 million for the same period last year. This represents the company’s 7th consecutive quarter of positive adj. EBITDA.

- Net income was a gain of $3.9 million or $0.03 per share, compared to a loss of $4.1 million or ($0.04) per share for the same period last year. This is the second consecutive quarter of positive net income, with the net income margin now up to 4%.

So again, it appears the profitability is continuing to trend in the right direction which is good to see. But it appears that the reason the stock was down following the Q2 results were due to the slower revenue growth.

Balance Sheet:

Now looking at the balance sheet, it remains healthy with cash of $72.1 million, no debt (as it just had leases) and a net cash position of $63.4M or $0.57 per share.

FY2025 Guidance:

Management reiterated its 2025 Outlook following the Q2 results, guiding toward mid-single digit revenue growth and Adj. EBITDA expected to be up 10%. So again, we are seeing growth in revenue moderating to some degree.

And on a valuation basis, today the stock trades at 12.4x forward EV/EBITDA – which in my opinion is starting to look much more reasonable than the other times I covered the stock.

But cash flow is still lagging so we unfortunately cannot get a gauge on the valuation when it comes to cash flow. And on a forward price-to-earnings multiple we are now looking at forward estimates with the business trading at about 34x earnings (so still not necessarily cheap).

So again, not screaming value, but each time I have covered the stock – with margins improving and the share price falling – it is getting more and more interesting.

Some other outlook comments from the CFO included – “We now expect roughly $8 million of gross tariff exposure in 2025 & For the second half revenue outlook, we will be lapping 2 large customer-specific promotional events with our 2 largest brick-and-mortar retailers that will not repeat this year.” And during the conference call it was indicated that Q3 revenue growth should be similar to that of Q2, and Q3 EBITDA will likely be below Q3 2024.

So again, although management has reiterated their guidance for the year, the profitability and revenue growth outlook for the second half of the year may be a bit weaker.

Conclusion:

- The company has a good track record of producing high single digit revenue growth – growing with a CAGR of 10% from 2019-2024 – and the business has increased margins now with 7 consecutive quarters of positive Adj. EBITDA and 2 consecutive quarters of positive EPS.

- The balance sheet remains healthy with net cash per share of $0.57 per share.

- Tariffs remain a risk, management indicates $8M exposure for the year, but they reiterated 2025 guidance 🡪 Looking toward 4-6% revenue growth & $27-$30M Adj. EBITDA. Nonetheless, management expects Q3 rev growth similar to Q2, and Q3 Adj. EBITDA to be down y/y.

The stock’s valuation is at about 12.4x forward EBITDA, but revenue growth is moderating in 2025. The business continues to get more appealing, but it currently faces some growth headwinds which In my opinion could keep the stock bound to its current range in the near to midterm.

YSOT Cipher Pharmaceuticals (CPH:TSX) – Viewer Request

| COMPANY DATA | |

| Symbol | CPH:TSX |

| Stock Price | $15.07 |

| Market Cap | $383M |

| Dividend Yield | N/A |

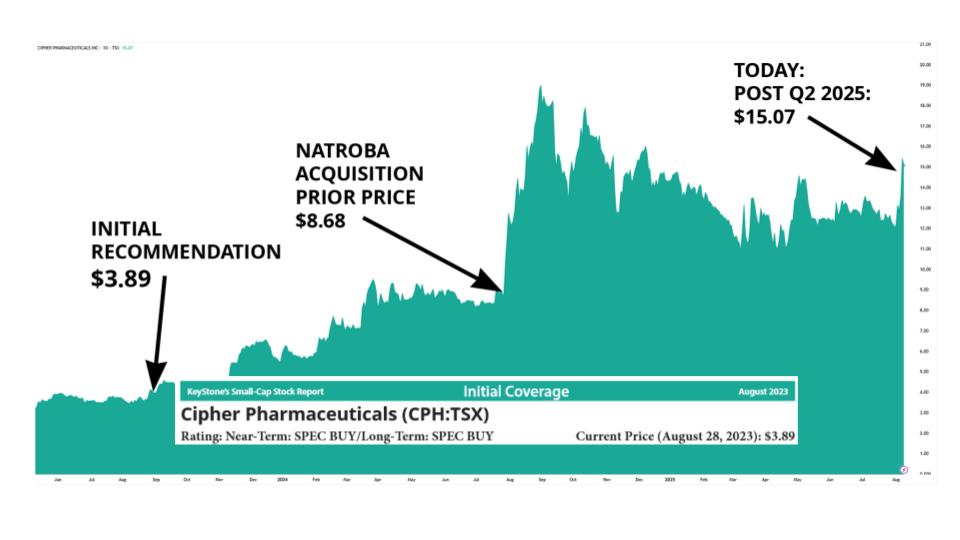

Cipher Pharmaceuticals CPH:TSX is a company clients should be familiar with. KeyStone recommended the company at $3.89 a share back in August of 2023, just under 2 years ago.

For those who don’t know:

Cipher Pharmaceuticals is a specialty pharmaceutical company with a portfolio of early to late-stage products. Core products include Epuris and Absorica in Canada and the US, and Natroba, which was acquired last year.

The stock is now trading at $15.07 a share, a $383 million market cap, a ~287% return since the recommendation just under 2 years ago.

A part of the initial investment thesis was cash deployment as the company was significantly cash rich at the time, roughly 52% of the market capitalization, with a cash-flowing product portfolio. We saw the cash deployment come about a year later with the acquisition of US-based Parapro and its lice and scabies treatment, Natroba. The acquisition was well received, sending the stock as high as $19. The acquisition was and still is a game changer for the company, but it does take time to see the benefits of the merger, and the benefits are being shown in the last quarter.

So, moving to the recent jump in share price off the back of the Q2, 2025 earnings. These results are lapping the last quarter prior to the Natroba acquisition, so we can see a nice before-and-after acquisition, effectively a year after the acquisition. I will not that Q3 will not fully be comparable either, as Natroba was acquired at the end of July.

But, Net revenue up 152%, to $13.4 million, gross profit up 159% to $10.9 million at a margin of 81.3%, Adjusted EBITDA up 148% to $7.6 million at a margin of 56.7%, diluted EPS up 83% to $0.22 a share. Overall, a substantial increase.

We have seen sequential quarter improvements to both Net revenue and Adjusted EBITDA since the acquisition took place.

Balance Sheet:

While the company is now in a net debt position of $14.1 million, compared to its prior net cash position, it likely won’t be for long, barring any further cash deployments. As you can see on the chart, there has been a consistent trend towards being net cash once again as the company has been actively paying off its debt, ending Q2 with $25 million left in debt, but after the quarter paid off a further $7 million. The company currently has a net debt to EBITDA of 0.9 times.

At this rate, it will only be 2 to 3 quarters until breaking into net cash once again. While the company did issue 1.5 million shares in part of the acquisition, causing the overall share count to increase year over year, the company has still been repurchasing shares, with $2.1 million or 230 thousand shares.

Overall, the balance sheet is still very strong given the strong cash flows, despite using cash, debt and shares to fund the acquisition last year. The company does have the ability to re-leverage itself if opportunities become available.

Which leads us to the growth prospects:

The company still has inorganic potential with products or companies given its balance sheet.

But the organic side is also very interesting at this time:

- Natroba has the potential to displace the current lice and scabies treatment Permethrin, which holds a ~75% market share, with Natroba at 25%. Notably, in April, Illinois updated there preferred treatment for Scabies and Lice to Natroba from Permethrin 5%.

- The company can out-license its current products internationally, specifically Natroba, for which management is currently looking for the right out-license partner.

- Then on the flip side, the company can look to in-license complementary products, as it does have a way to market products within both the US and Canada now.

- Lastly, the company can bring its products across the border, likely Natroba into Canada.

Depending on the time of any in-licensing, out-licensing or acquisitions, we could see future quarters of jumps in sales and profitability, but that depends on what exactly occurs.

Valuations:

The company is trading at

- A trailing P/E of 23.0 times

- A EV/EBITDA of 12.9 times

- And a P/FFO of 20.0 times

Conclusion:

We continue to like Cipher Pharmaceuticals despite the significant price increase since the recommendation. The company has obviously increased in valuation, but at recommendation, it was a very cash-rich company awaiting deployment of that cash, and now it has both organic growth, which it previously did not have in its financials, given the mature product portfolio, as well as further acquisitions or licensing opportunities. And the opportunities are supported by the continued strong cash flows and an improving balance sheet.

Clients will be receiving a full update in the near future.

KeyStone and KeyStone employees currently own the stock