Beyond the S&P 500: Finding Overlooked Opportunities in Small Caps

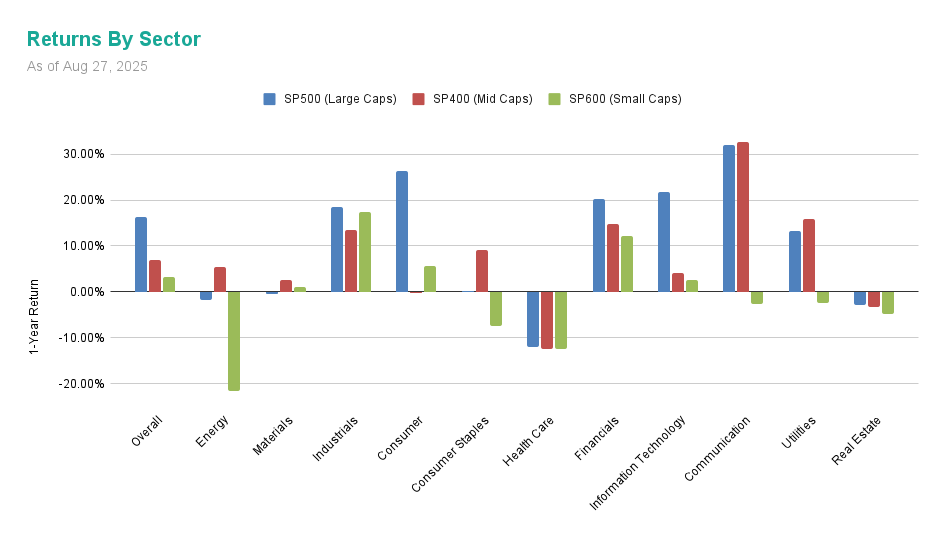

Large caps have continued the dominance of returns over small caps over the past 12 months, with the large cap, S&P 500 returning 16.4% compared to the small cap, S&P 600’s 3.3%. But we can dive deeper into what is driving these indices by sector, and further look across market capitalization by various indices. Investors can look at these figures to help examine potential areas where great companies may have been thrown out with the bath water, creating potential opportunities. As well, examining what makes up the indices can provide valuable insight.

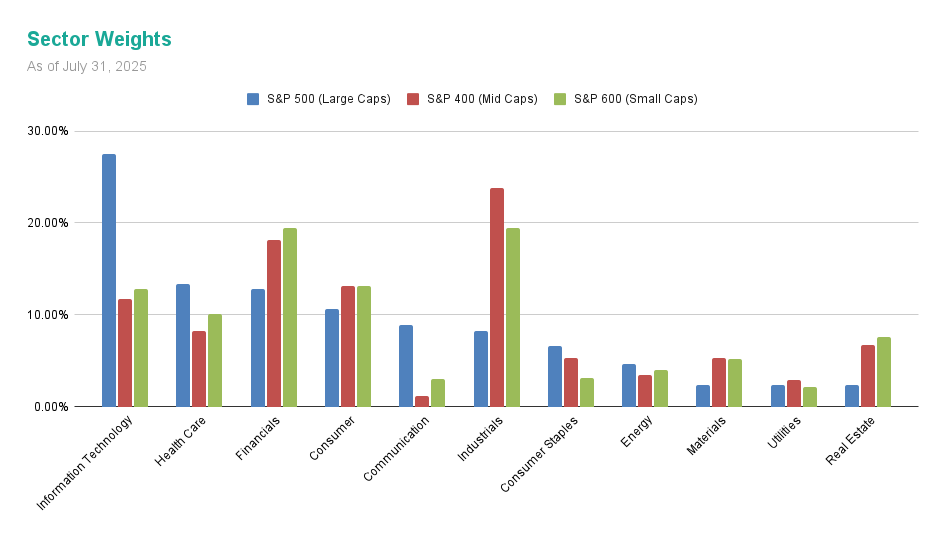

Due to the examined indices being weighted by market cap, which is common practice, the sector concentration varies substantially. The S&P 500 is weighted significantly towards Information Technology while the S&P 400 and S&P 600 skew towards Industrial and Financials. The sector skew can impact overall index return returns when a sector is in or out of favour. Further, the S&P 500 is more top heavy, dominated by the major players. The top 10 holdings for the S&P 500, S&P 400, and S&P 600 represent 30.6%, 7.3% and 6.3% respectively. The S&P 500’s top holding, Nvidia (NVDA:NASDAQ) comes in at 7.3% of the overall index weight, resulting in a degree of concentration in a single name.

Small caps have under performed across nearly every single industry with the only exception being materials where large caps fell 0.4% compared to small caps gain of 1.1%, a relatively minor difference. Driven by the highest return in the S&P600, the rare earth metal producer ![]() MP Materials (MP:NYSE) with a whopping 488% gain. This gain stemmed from significant American change towards self produced rare earth metals in light of China, who produces over 90% of rare earth ore implementing strict export restrictions. Further driven higher by a $500 million deal with Apple (AAPL:NASDAQ). The initial catalyst was completely out of MP Materials hands, but is structured to benefit from the geopolitical shifts.

MP Materials (MP:NYSE) with a whopping 488% gain. This gain stemmed from significant American change towards self produced rare earth metals in light of China, who produces over 90% of rare earth ore implementing strict export restrictions. Further driven higher by a $500 million deal with Apple (AAPL:NASDAQ). The initial catalyst was completely out of MP Materials hands, but is structured to benefit from the geopolitical shifts.

Communication Services mid & large caps both well outperformed the other subsegments of the market. The large caps were driven by great returns in Netflix (NFLX:NASDAQ), and Live Nation Entertainment (LYV:NYSE), with the mid cap returns heavily driven by EchoStar’s (SATS:NYSE) ~230% return after being bought out by AT&T (T:NYSE). The small caps were weighed down by big losers like TechTarget (TTGT:NASDAQ) falling 78%. Even though indexes are generally seen as a diversification, when looking at sector analysis they can become much more concentrated as the amount of holdings per sector can be low, magnifying the impact of losers and winners. Further, it should be noted that the overall weight of the Communication Services in the SP400 is the smallest out of all the sectors at only 1.2%, so even though it was the index’s top performing sector it is also the lowest weight.

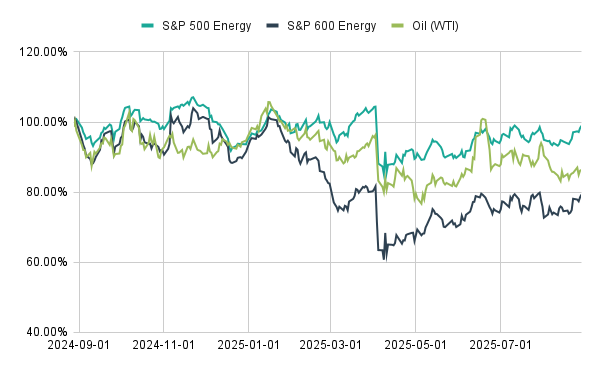

Small cap energy stocks had a notable underperformance with a sharp decline of 21.5% compared to a large cap decline of 1.7%, a 19.7% spread between the two. With oil prices declining over 14% over the past year, it is no surprise energy stocks have declined, but small cap energy stocks within the index have been pressured further by leverage levels with generally less flexible balance sheets and operations more sensitive to the immediate shift in oil prices. During, the geopolitical instability since the start of the year oil has declined but the small-cap energy companies have fallen at an accelerated pace. The big shock in the WTI and Oil equities was the Liberation Day Tariff announcement which slammed the sector. Energy equities have partially recovered since, but small caps remain well below the start of the year.

A small cap energy producer KeyStone recommended just last year has since returned over 50%, a core difference being the strength of the balance sheet as well as the idiosyncratic long-term growth potential. Companies like this are not in major indices, and often are overlooked by investors. Even in a declining sector there are winners, Wallstreet commonly overlooks great small caps as they are not large enough for many institutional investors nor need to raise capital, leaving them ripe for the picking for individual investors. Canadian Small Cap and VIP clients have access to research on this high potential oil and gas investment.

Access KeyStone’s 2025 Cash Investment Product Report

Explore the safest, highest-yielding places to hold excess cash—ISAs, T-Bills, GICs, and more—all available inside your brokerage account.

Shifting to a sector with near-parity returns, there has been a broad decline in the Health Care sector all declining ~12% across market caps. Some notable losers being the health insurers, United Healthcare (UNH:NYSE) and Centene (CNC:NYSE), losing 48.6% and 63.7%, respectively over the past year. The troubled insurers have faced a series of challenges, with regulatory and public scrutiny and poor financial performance driven by declining margins. Many investors including Warren Buffett’s Berkshire Hathaway have now taken a position in the struggling insurer United Healthcare. While the investment has created buzz and hope for many, the stock is still over 50% from its all time highs, and is still pressured by internal and external factors.

Over the past year one of KeyStone’s picks, ![]() Biosyent (RX:TSXV), a specialty pharmaceutical company, returned 9%, with a 1.7% dividend yield as well. The company offers recession resilient products reducing overall risk compared to other pharmaceutical companies. The company’s main product is FeraMAX 150, an oral treatment for iron deficiency. A key financial feature of Biosyent is the strong net cash position, with roughly 20% being cash or $2.34 a share. The strong cash balance allows for financial flexibility for shareholder returns via dividends and share buybacks as well as organic and inorganic growth. The company boasts a robust track record of 60 consecutive quarters of profitability which a track record of that length is not guaranteed for small cap companies. The growth prospects remain high with 14% sales growth, and 28% net profit growth over the past year. Further, the valuation remains reasonable at a ex-cash P/E of 13 times. At a ~$135 million market cap and $11.79 a share, you won’t find this company in any large index.

Biosyent (RX:TSXV), a specialty pharmaceutical company, returned 9%, with a 1.7% dividend yield as well. The company offers recession resilient products reducing overall risk compared to other pharmaceutical companies. The company’s main product is FeraMAX 150, an oral treatment for iron deficiency. A key financial feature of Biosyent is the strong net cash position, with roughly 20% being cash or $2.34 a share. The strong cash balance allows for financial flexibility for shareholder returns via dividends and share buybacks as well as organic and inorganic growth. The company boasts a robust track record of 60 consecutive quarters of profitability which a track record of that length is not guaranteed for small cap companies. The growth prospects remain high with 14% sales growth, and 28% net profit growth over the past year. Further, the valuation remains reasonable at a ex-cash P/E of 13 times. At a ~$135 million market cap and $11.79 a share, you won’t find this company in any large index.

Whether in the Canadian or American markets, looking at individual stocks is difficult, let KeyStone help you in discovering unique investment opportunities that you will hear about nowhere else. Become a client today to being building your simple 20-25 stock portfolio.