You are listening to KeyStone’s Stock Talk Podcast – Episode 306

This week, I will kick off our YSOT segment answering a viewer and client question on Bowman Consulting (BWMN:NASDAQ), an engineering services and program management firm which is up 60% year to date and has returned our US Small-Cap clients over 110%. I will let you know what is driving the stock. Second, Brett takes a look Roblox Corporation (RBLX:NYSE), which operates a user-generated online gaming platform where users can create, share, and play games developed by a global community – the stock has been on this year and Brett let’s you know if the cash flow currently stacks up to the hype. And, last but not least, Aaron gives his take on global CRM leader, Salesforce Inc. (CRM:NASDAQ).

Let’s get to the show – we welcome my cohosts, Mr. Aaron Dunn and one half of the killer B’s, Brett.

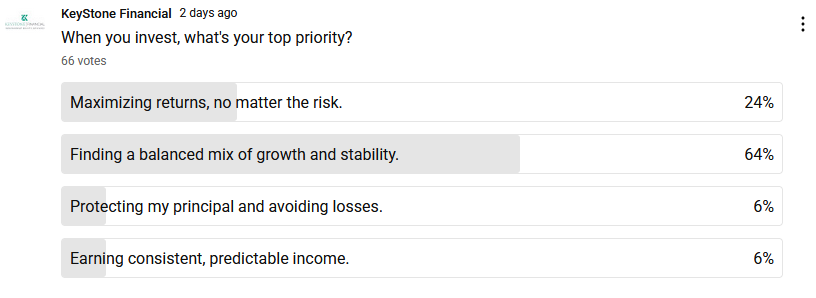

Poll Question

YSOT Bowman Consulting Group Ltd. (BWMN:NASDAQ) – Viewer Request

| COMPANY DATA | |

| Symbol | BWMN:NASDAQ |

| Stock Price | $39.74 |

| Market Cap | $689.34M |

| Dividend Yield | N/A |

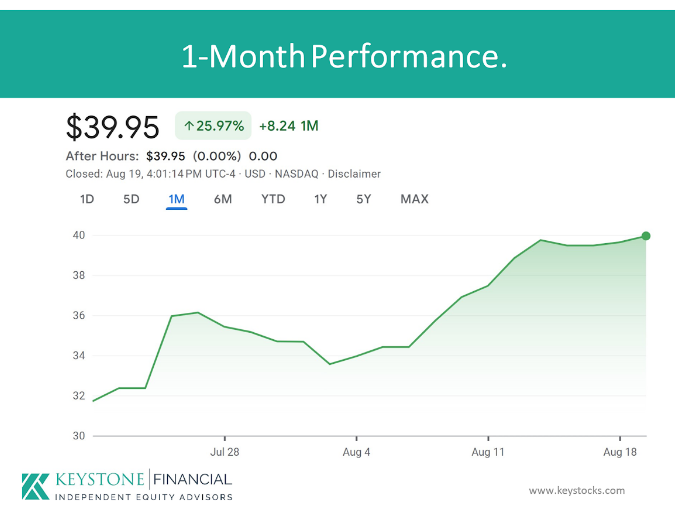

Clients of KeyStone’s US Small-Cap Growth Stock research should be familiar with Bowman as it has performed well after being recommended at $18.84 and today trading at just under $40, up 111%.

What makes Bowman different from many construction or engineering firms?

Key Differentiators

- No General Contracting: Unlike many engineering firms, Bowman does not engage in general contracting or design-build projects. This strategic decision helps them avoid the financial risks associated with construction delays, cost overruns, and liability for a project’s physical completion. Their role is to provide the expert planning and design services, not to execute the construction itself.

- Service-Based, Low-Inventory Model: Bowman’s business is centered on providing intellectual and technical services. They don’t carry significant equipment inventory or physical assets that could devalue or create financial risk. Their primary costs are internal labor and other professional expenses, which are more predictable and controllable than the capital costs and variable expenses of a contracting firm.

- Strategic Acquisitions: Bowman’s growth strategy is heavily based on acquiring other engineering and consulting firms. This allows them to quickly expand their geographic footprint, diversify their service offerings, and add new talent and clients without the long-term, high-risk capital investments of organic expansion

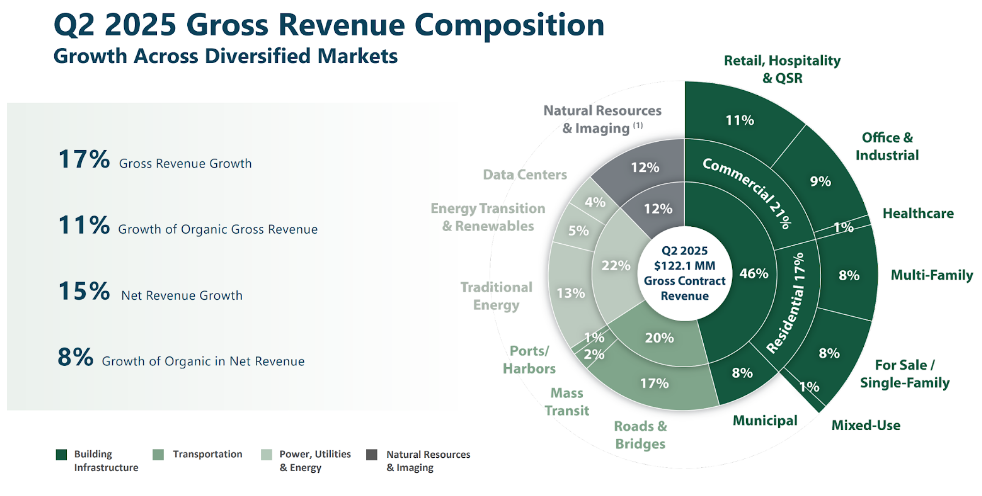

Revenues are derived from 4 core areas: Building infrastructure by far the largest at 46% in Q2 – consisted of 21% commercial and 17% residential in quarter, 22% Power, utilities and energy – consisting of traditional energy (still makes up the most) energy transition and renewables, and Data Centers which are growing at present, 20% Transportation – consisting primarily of roads and bridge work, and 12% finally Natural Resources Imaging.

Let’s look at the stock over the past month:

Year:

What is driving the share price performance? A number of things, but it starts will strong financial performance.

Increased guidance drives share price higher…

Rationale for Raised Guidance

- Strong Demand and Bookings: The company experienced robust demand across its core verticals, particularly in Transportation, Renewables, and Energy Transmission. This demand translated into record bookings during the second quarter, resulting in a book-to-bill ratio exceeding one. Management has also reported that bookings in the third quarter are already surpassing those of the second quarter, indicating sustained momentum.

- Record Financial Performance: The record-setting gross and net revenue, along with Adjusted EBITDA in Q2 2025, reinforces management’s confidence in achieving the full-year targets.

- Operating Leverage and Margin Expansion: The company is observing a “scale effect,” where revenue growth outpaces overhead expansion. This is leading to margin improvement, attributed to disciplined labor cost management and optimized workforce utilization.

- Diversification and Organic Growth: Bowman continues to benefit from the diversification of its revenue streams and strong organic growth across all verticals. Notably, Transportation grew by 21%, Natural Resources & Imaging by 19%, Power Utilities and Energy by 5%, and Building Infrastructure by 4%.

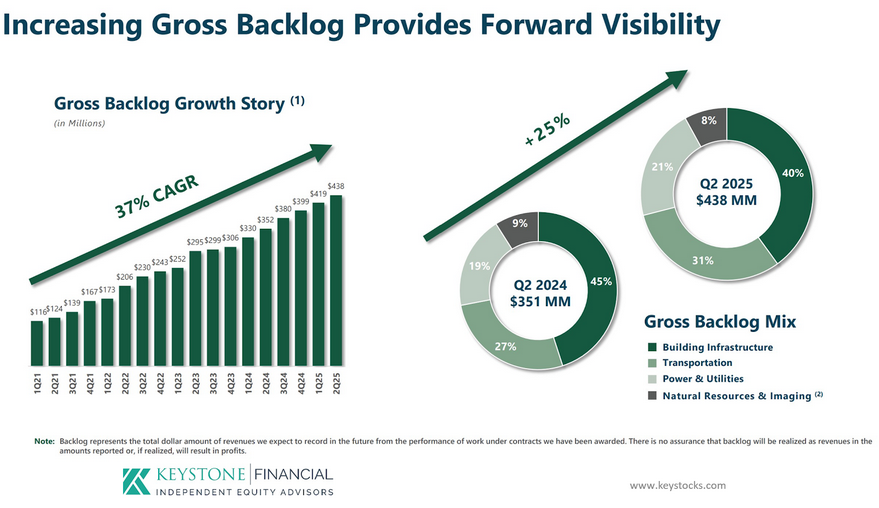

- Healthy Backlog: The substantial 24.7% growth in gross backlog provides significant revenue visibility for the remainder of 2025 and into early 2026, underpinning future performance.

Valuations:

But if you recal the last quarter the company went from a loss position to a significant profit – we think the PE will move lower quickly.

For example, in Q2 – GAAP Basic EPS improved to $0.25 in Q2 2025 from a loss of $0.24 in Q2 2024On a non-GAAP basis, Adjusted Diluted EPS reached $0.55 in Q2 2025, significantly outperforming the prior year’s $(0.03) and exceeding analyst estimates.

Price/Cash Flow (P/CF) Ratio: The TTM P/CF ratio is in the range of 20. Not overtly high for a company with organic and acquisition growth.

Conclusion:

- Quality business, well run with a growing backlog – both organically and via acquisition.

- Valuations appear higher, but are quickly moving lower.

- Clients will be updated with our new rating over the next 10 days.

YSOT Roblox Corporation (RBLX:NYSE) – Viewer Request

| COMPANY DATA | |

| Symbol | HNST:NASDAQ |

| Stock Price | $117.25 |

| Market Cap | $81.3B |

| Dividend Yield | N/A |

Roblox Corporation, symbol RBLX on the NYSE operates a user-generated online gaming platform where users can create, share, and play games developed by a global community. The company generates revenue primarily through the sale of its virtual currency, Robux, as well as advertising partnerships and premium subscription services.

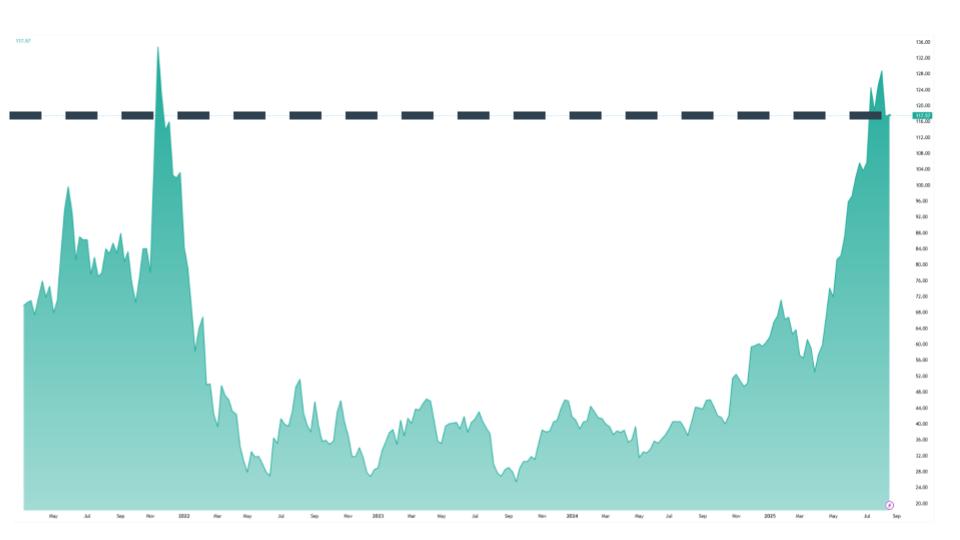

The stock has had a very strong year, up 187%, the stock is trading at $117.25 a share, with a $81.3 billion market cap. Although the stock has fallen off its high at the end of last month after its Q2 earnings.

However, if we zoom the shares are still just in the same range as it was during the 2021 mania price. So, shareholders who invested at or just after the IPO haven’t had as great a return, at least yet.

First up, the most recent financials:

Revenue was up 21% to $1.08 billion, driven by significant growth in active users and bookings per active user.

Bookings were up 51% to $1.44 billion.

Operating loss was $322 million compared to a loss of $238 million.

Adjusted EBITDA was down 72% to $18.4 million. The major factor between adjusted EBITDA, and operating loss is the stock-based comp. Of which the company expense $285 million during the quarter.

EPS fell to a loss per share of $0.41 from a loss of $0.32.

Key performance indicators, hours engaged rose 57% to 27.4 billion hours, daily active users rose 41% to 111.8 million, and average booking per daily active user rose 7.1% to $12.86. Average booklings per user does have seasonality with Q4, being stronger, but the general trend has been increasing, but not as linearly as the other metrics, which is expected/

As well concurrent users have pushed past 30 million users, with management noting 20 million concurrent users playing grow a garden. Daily user growth had high engagement with 5 games Grow a Garden, Steal a Brainrot, Brookhaven, 99 Nights in the Forest and Ink Game. Of which 4 of 5 were launched in the last 12 months. This is a key aspect to Roblox’s environment since it needs a constant churn of new popular games to drive user growth. This, in turn, requires attracting developers and brands that cater to the audience to hit its targeted 10% of the global gaming content market.

As well, in the couple of graphs I have up, you can see the 13 and over category has risen at a faster rate for both the hours engaged and daily active users. This is something management has been targeting to age up the platform. Overall, strong user growth.

Balance Sheet:

Shifting back to the financials, the balance sheet is great, cash-rich. Holding $4.7 billion in cash and investments, which are composed of government debt and money market funds long-term and short-term. With 1.6 billion in leases and debt, leading to a net cash position of $3.1 billion.

As the bookings are upfront payments, the company benefits from receiving cash up front before revenue and the related costs are recognized. But this leads to a massive deferred revenue liability of $5.1 billion. This can create a drag on cash flows if revenues exceed bookings. If the Robux, the in-game currency, is spent and then redeemed by developers, the company will see the opposite of what is occurring now, cash outflow. Not the case right now, but that is the risk in having significant deferred revenue.

2025 Guidance:

- Shifting to the guidance for 2025,

Revenue of $4,390 to $4,490 million, 22 to 25% growth - Bookings of $5,870 to $5970 million, 34% to 37% growth

- A net loss of $1261 to $1201 million, shifting further into a loss, compared to $941 million.

Effectively breakeven adjusted EBITDA, at a loss of $5 million to a positive $55 million, compared to positive EBITDA of $180 million for 2024.

Free cash flow of $1025 million to $1085 million, 60 to 69% growth.

Valuations:

Now using those metrics, for some forward valuations from the midpoint. Forward price to sales comes in at 18.3 times, and forward price to free cash flow comes in at 77 times. Neither cheap.

Conclusion:

The user Key performance indicators are strong, all growing at high rates, but that hasn’t been reflected in profitability for the company only revenue and bookings. Cashflows look better due to the nature of the business and the high stock compensation. But the company is trading at a significant multiple with respect to sales and free cash flow, the 2 better-performing financial metrics. Growth upside seems to be largely accounted for, and profitability is not there yet, so we will continue to monitor to see if the company can shift into profitability and then actually look to grow the profitability on a per-share basis.

And as for a disclosure, KeyStone and KeyStone employees have no position in Roblox